A Recession Rain Delay and The Peak in the Markets Soft Landing Thesis

A Recession Rain Delay and The Peak in the Markets Soft Landing Thesis

The Fed has officially Pivoted. The market is excited. Don't get carried away in its FOMO (Fear of Missing Out).

Cartoons of the Week:

The Fed Pivot

Long time, no write. It has been a while.

I hope everyone is doing well. I took a brief hiatus from these weekly writings due to time constraints with coaching my son’s football team. After a fantastic season, where we went 7-2 and made it to the league championship, I am setting my sights again on writing.

I was going to wait till the new year to start writing again but this week’s news compelled me to put this brief snapshot together.

If you have not been following the news, this week we officially received the “FED PIVOT”!!!

This move to a pivot is a head-scratcher, in my view.

Not long ago (2 weeks to be exact), the chair of the Fed was talking about how premature it was to discuss Fed rate cuts.

Now the Fed has forecasted, through its dot plot, 3 rate cuts in 2024.

And in good old market fashion, this means the market is now pricing in 6 rate cuts in 2024!!!

To add to my confusion, this morning John Williams, the head of the Federal Reserve Bank of New York, and permanent voting member of the Fed, said the following:

While I am not going to go into the merits and details of why I find this so confusing, I did want to talk about a few quick things to keep in mind as we enter 2024.

The soft landing thesis is ALWAYS the focal point after the Fed stops raising rates.

But, as outlined in this Bloomberg article below, true soft landings are very rare.

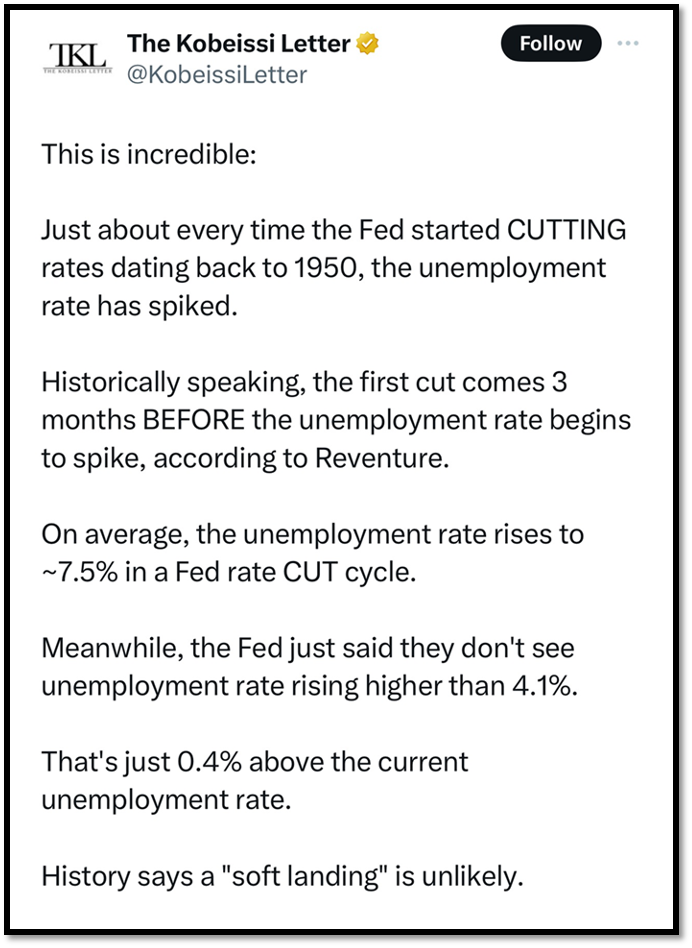

The soft landing thesis of 2023-2024 is hanging its hat on the strong employment market we are currently experiencing.

What people seem to have forgotten is the fact employment is the ultimate LAGGING indicator. It is usually the last thing to break.

Using history as our guide, you can see below, going back to 1950, we have never seen employment move higher UNTIL after the Fed started to cut rates.

And while it looks strong today, LEADING indicators for employment are showing a gloomy future.

The issue with employment weakening is the fact when it starts, it usually does not stop.

It becomes a negative feedback loop that looks something like this:

Customers slow their spending (happening now),

Corporations feeling the pressure, look to cut costs (usually employees, I predict first to second quarter of 2024 we will see this escalate)

Once people lose their jobs, their spending habits change dramatically (mid-2024 story)

Corporations and businesses seeing the cut in spending, look to cut costs even more by laying off more people.

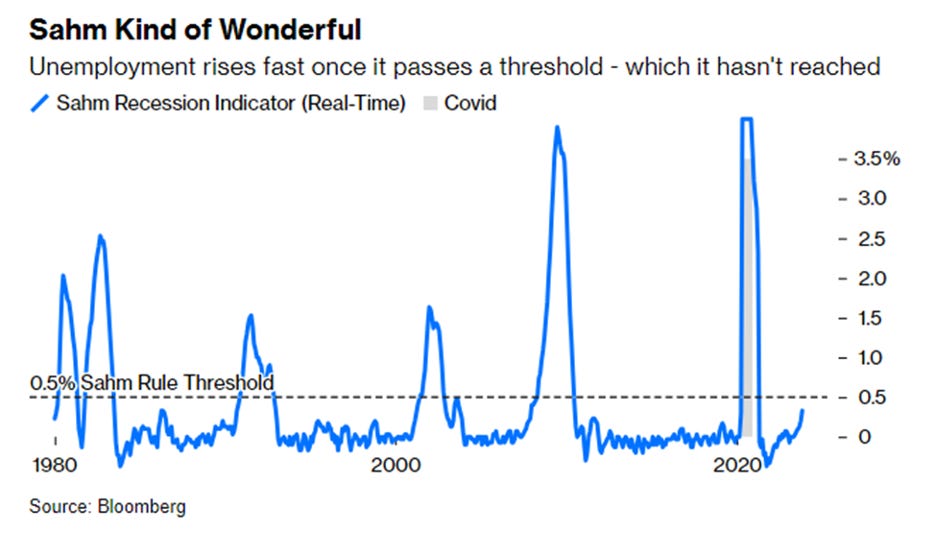

If I am right, by mid-2024, we will see a big change in our economic picture and the Sahm Rule recession indicator screaming the big R word.

Another thing to keep in mind besides employment is the fact the market, historically, does not bottom until the Fed starts to cut rates.

To me, it is hard to see how we do not follow history on the timing of the 2-year yield prediction of a recession, the slow and then sudden demise of the employment market, and ultimately the negative impact both of these will have on the equity market in 2024.

Unless this time is truly different….Maybe it is. But I have not capitulated just yet.

With this in mind, here is my wildly out-of-consensus prediction of the equity markets and politics in 2024:

“In 2024, we will make new highs in the market. Those new highs will not last long and will collapse under the pressure of weaker earnings, weaker consumer spending, weaker employment, higher defaults, and a global economic slowdown. We will then see a 20% plus correction, highlighting the year of the “blow-off top”.

The bond market will show a healthy positive return, insulating some of the negative returns we will see in stocks. Rates will move lower to counter the economic slowdown. As we move out of this downturn in late 2024, early 2025, that ugly thing called inflation will pick up steam again.”

“On the political front - deep gulp - if this thesis plays out, Biden will not get re-elected. BUT, I do not see Trump being the new President in 2024. Frankly, I think he may (sorry for those that like him) drop dead before that time. Our new President in 2024 will be Nikki Haley.”

Crazy right….Remember, it’s only a prediction.

A real-time picture of me on Bear Market Island typing away this note. Bear Market Island is a very lonely place at the moment.

Final Thoughts……

Way back in February 2023, I wrote an article titled “The Topics of Soft Landings, Hard Landings, Recessions, and Unemployment in 5- Minutes or Less..Ready...GO.”

https://enlightenedamadan.substack.com/p/the-topics-of-soft-landings-hard

In this article, I highlighted the historical timeline the market usually takes after the Fed stops raising rates. This analysis specifically revolved around the 2-year yield.

Back in February 2023, I felt we were near the end of the Fed tightening cycle, and close to the Fed Pivot.

Using the 2-year yield as our guide, the article stated once the yield peaks, the game of timing the recession begins.

As you can see below, that article timed the peak in the 2-year yield (at that time) within 2 weeks.

But then a funny thing happened in June. The 2-year yield began to rise again, taking out the March highs in September and continuing to rise through October.

This unexpected rise in the 2-year yield set in place what I would call a “rain delay”, 6-months into our timing of the recession game.

In September, the game was canceled and rescheduled to start again in late October, when again, the 2-year yield peaked.

Because of this delay, I highly recommend everyone take a second look at that article I wrote back in February of 2023 and apply it to today.

While 2023 caught me and many others off-guard, the Fed Pivot this week and rolling over of the calendar to a new year does not mean we are out of the woods just yet.

I will leave you with comments from Marko Kolanovic, the JP Morgan analyst on what he feels 2024 may look like

From JP Morgan Research Marko Kolanovic:

“Finally, we want to point out that it is becoming consensus thinking that a recession will be avoided. We see the arguments such as no landing, goldilocks, election year seasonality, labor market resiliency, up-rating of valuations, Fed put, etc., as various versions of “this time is different.” Going back to basics and the relatively small number of recessions we can study – signaling from yield curve inversion indicates that recession risk is highest between 14 and 24 months following the onset of inversion. That period will cover most of 2024 and should make it another challenging year for market participants.”

Thank you, from the bottom of my heart, for making this publication a success and spending the little bit of your precious spare time you have reading my insights.

I will be back to the grind in 2024 providing weekly market insights, education, analysis, and more.

I hope you all have a very Merry Christmas, a fabulous holiday season, and a wonderful New Year.