A Recession is Coming!? Says Who....

A Recession is Coming!? Says Who....

Friday Financial - Week 29, 2022 - What is a recession, what needs to change to push us into one, and who ultimately decides

(15-minute read time)

Cartoon(s) of the Week:

Quotes of the Week:

“A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators.”

-National Bureau of Economic Research Committee

“We are going to have a very unusual conflict between the employment numbers and the output numbers for a while.”

-Robert Gordon Northwestern University economics professor

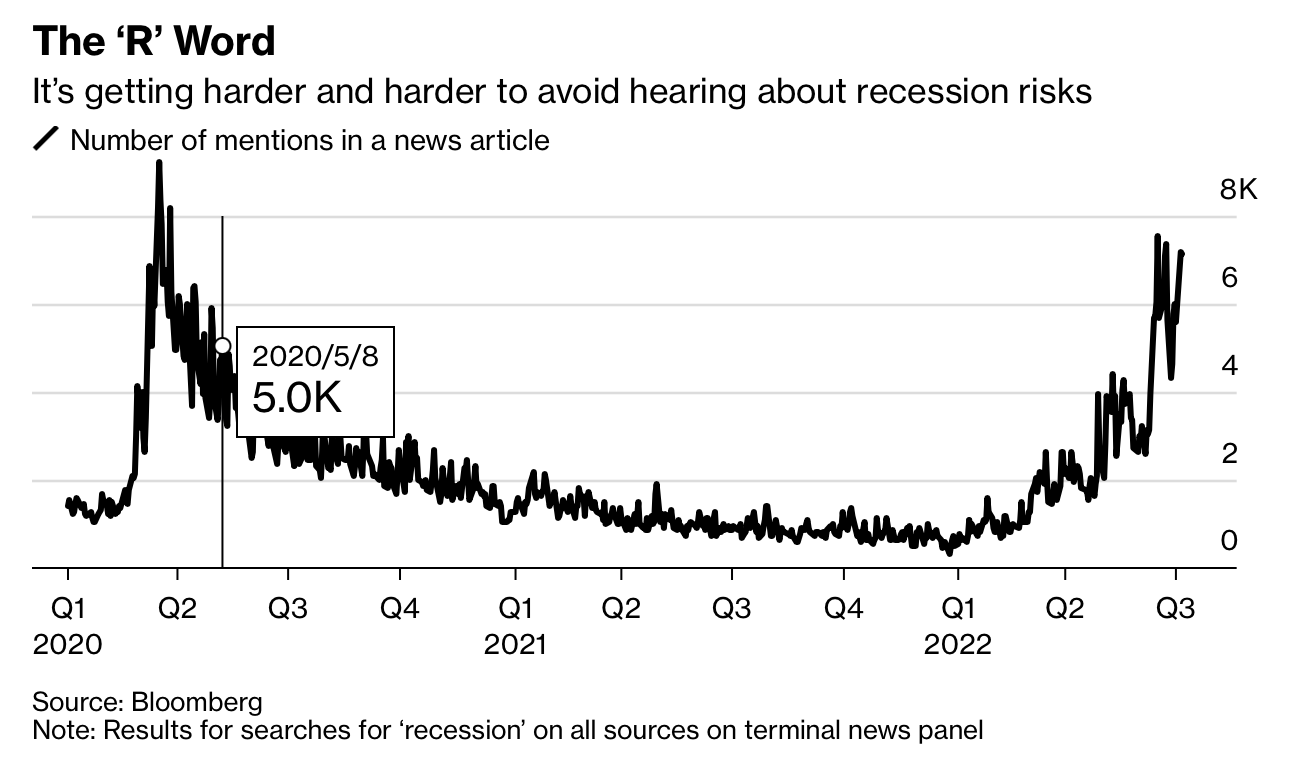

Wherever you turn today, you will hear the loud ramblings of the “R” word.

The New York Times did a full page picture article on July 21 outlining the risk of a big “R” coming soon.

Most other forms of media (some more than others depending on their political tilts) have had specials or large write ups about the big “R” word that is coming.

While I am in agreement we are in the middle of a downturn and potential “R” word, we are in one of the most unusual economic times in history.

As we get closer to the November elections, you are going to be hearing a ton more about the big “R” word as politicians, bankers, and others jockey for talking points.

But before all this hits the daily headlines, I wanted to help educate you on what the heck the “R” word really means and why it may get very complicated over the next 3-6 months.

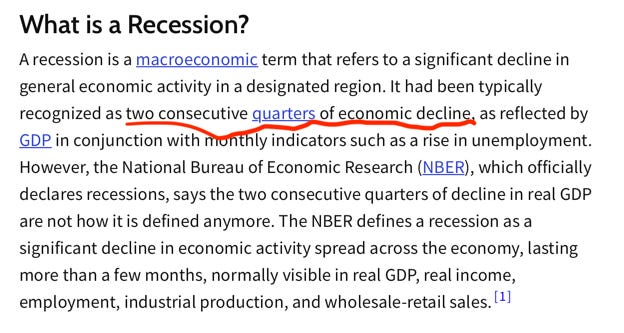

What is a Recession?

If you remember Econ 101 from high school or college, you probably remember the term outlined below from Investopedia.

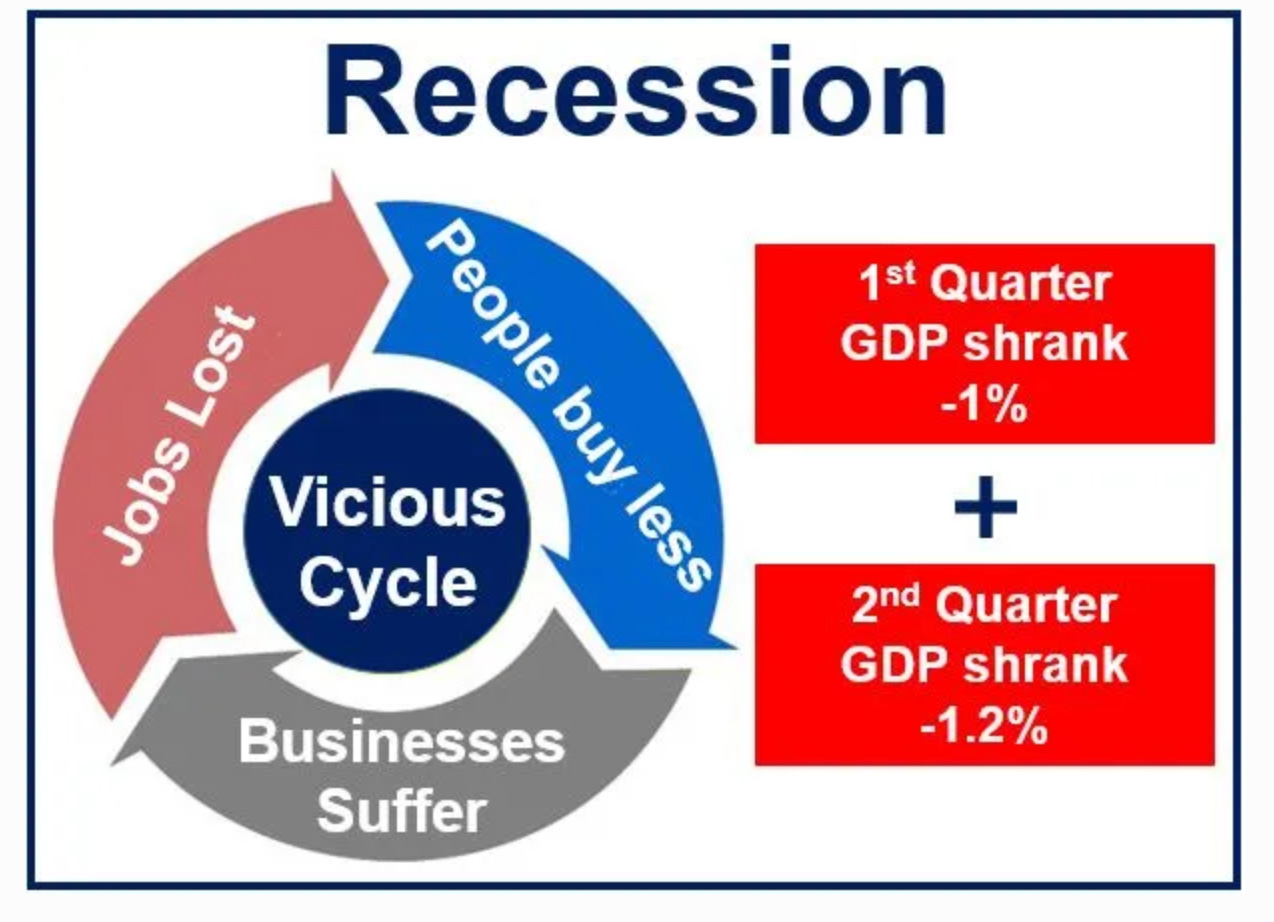

A recession per our old Econ text books is “two consecutive quarters of economic decline”.

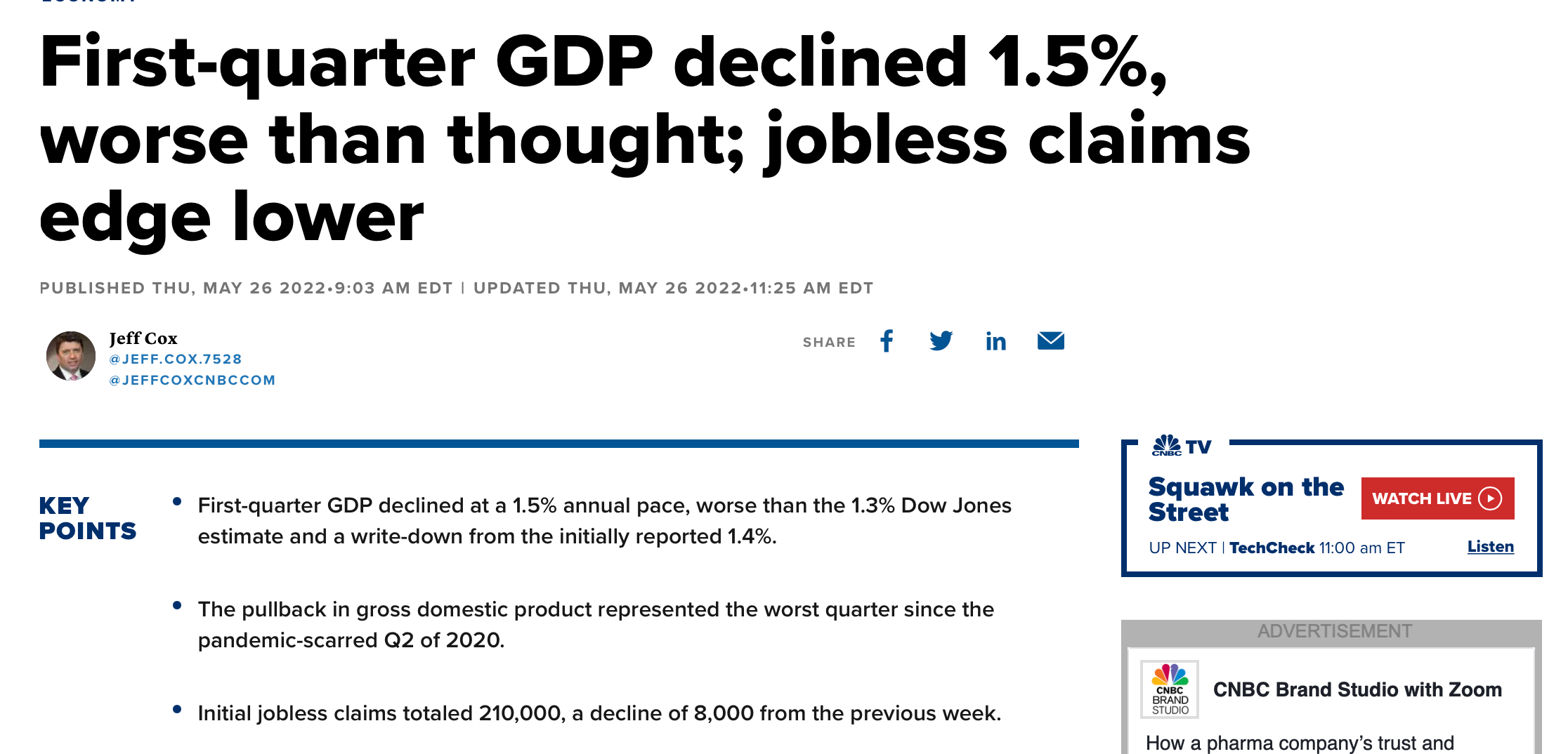

Looking at the first quarter (Jan through March 2022), we printed a negative GDP number.

And if we use the Atlanta GDP now viewpoint for the second quarter below, which shows current second quarter GDP (April through now) at a -1.6%, then we are in fact in a recession, right?

Well, as one of my all time favorite football commentators Lee Corso usually says,

“NOT SO FAST!!!”

As Anna Wong, Bloomberg chief US economist recently stated,

“Q1’s contraction is mainly due to strong imports (due to strong demand) after slowdown inventory building due to combination of supply bottlenecks and gangbuster inventory building in Q4 last year. It’s hard to interpret that as a weakness-driven contraction.”

Leave it to economist to complicate the easy and make it hard.

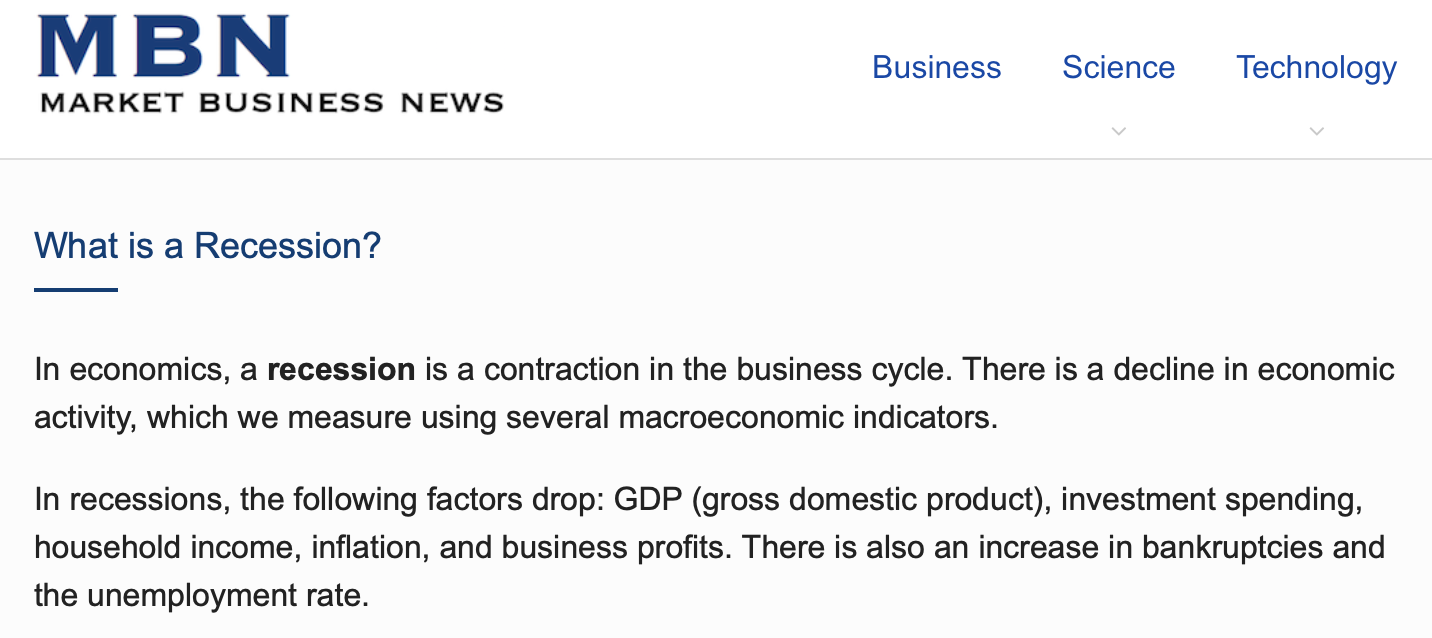

The More Complicated Definition of a Recession

While most would argue the two consecutive quarters of negative GDP is good enough to say we are in a recession, this is not the real definition.

The Market Business News website outlines their definition of a recession.

They say its a “contraction in the business cycle” that is “measured using SEVERAL economic indicators”.

Forbes Article from July 12th titled “What is a Recession” outlined the indicators that go into the “recession” call.

They mention several economic indicators including “rising levels of unemployment.”

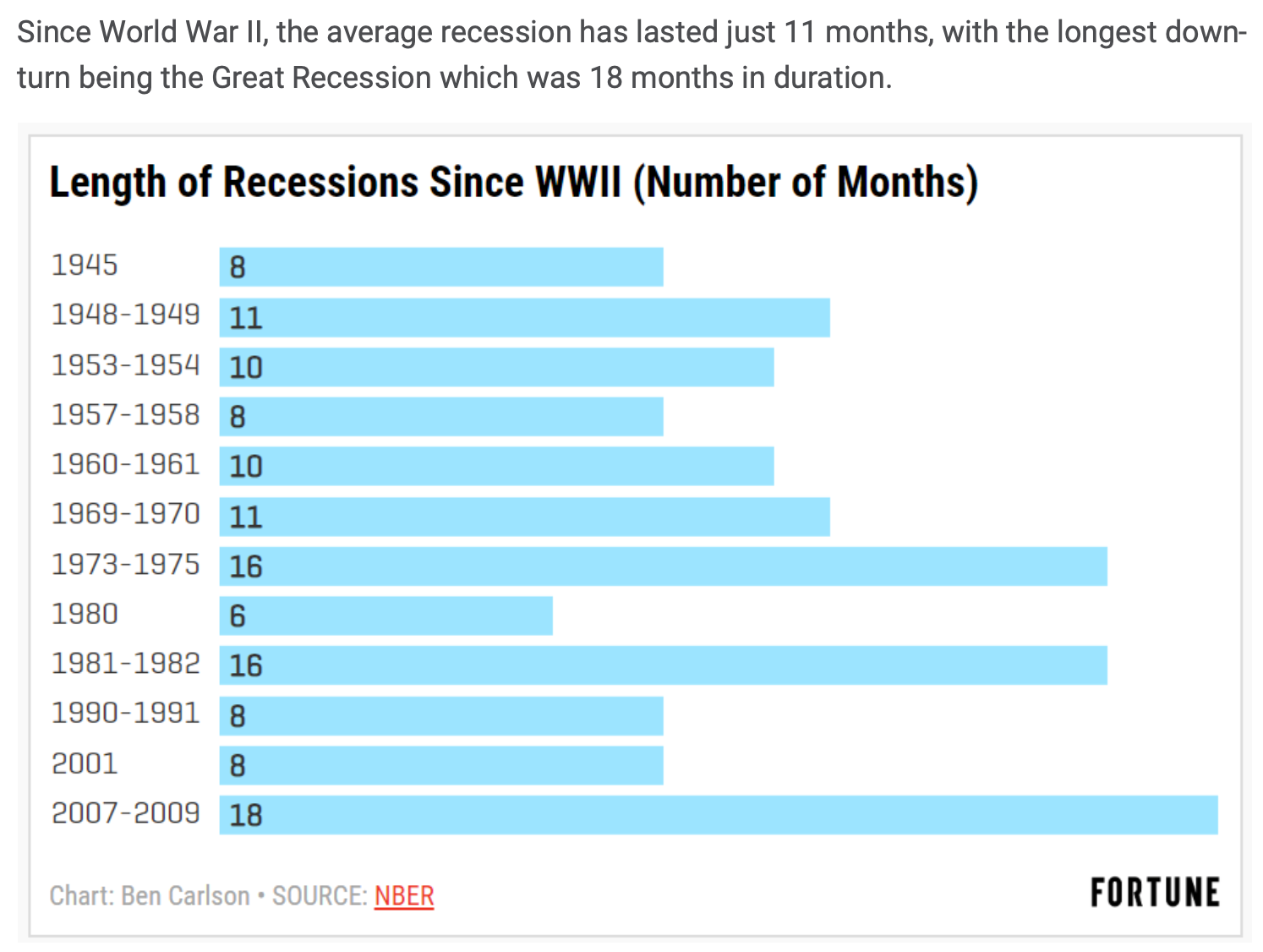

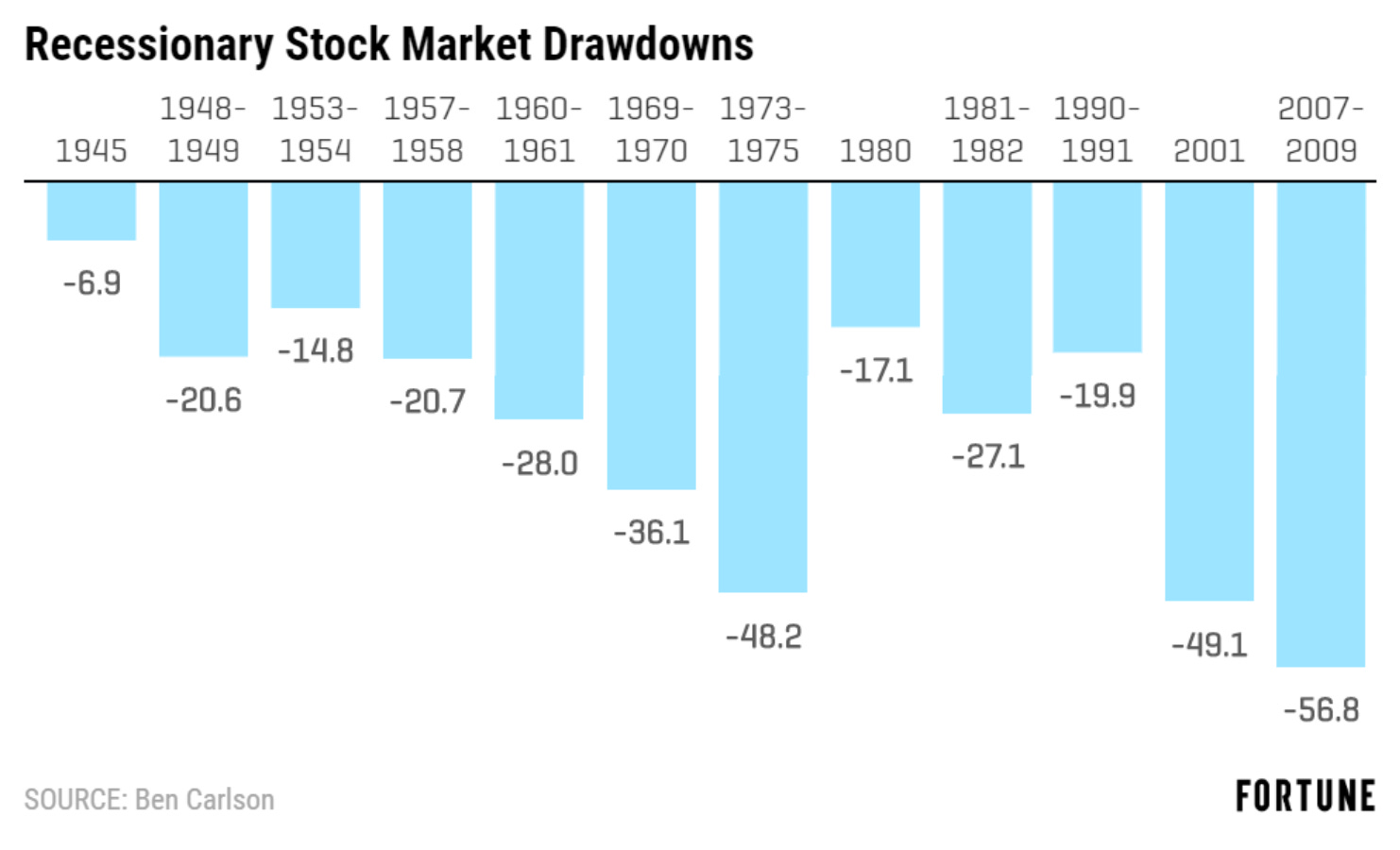

History of Recessions

Our economy has experienced 12 recessions since World War II. All of them have seen economic output contract (think negative GDP, industrial production moving lower, consumer spending slowing down) ALONG WITH a rise in unemployment.

Usually these moments in history have been some of the most difficult for you, your family, and your friends. It’s the economy moving in reverse, and usually has most people feel economic and financial stress.

Symptoms include checking your brokerage statements daily as the losses mount, or seeing your big cash cushion you thought you had in your house or business vanish into thin air.

Some of the bigger risk takers will see those speculative assets that made them a ton of money over the previous few years reverse in value eventually losing 70-100% of their original value. As most of those speculators have been rewarded in the past for buying the dip, now these speculators have nothing left to buy the big dip and are poorer then when they originally started.

Those who are employed and do not lose their job see their overall pay move lower at the same time they are forced to do the job that took two or three people in the past to do. But, at least you have a job right…

Recessions usually force you to make extremely hard financial decisions.

In some of the worst recessions like 2008, you get this overall feeling of pain in your gut and the constant thought of just wanting to jump out a window. (at least that was me when trying to manage the volatility in the hedge fund I managed).

Sometimes its relentless while other times it’s quick.

No matter which recession was the worst for you over the last 80 years, all of them had similar characteristics of a down stock market, lower housing prices, slowing economic production, and rising unemployment.

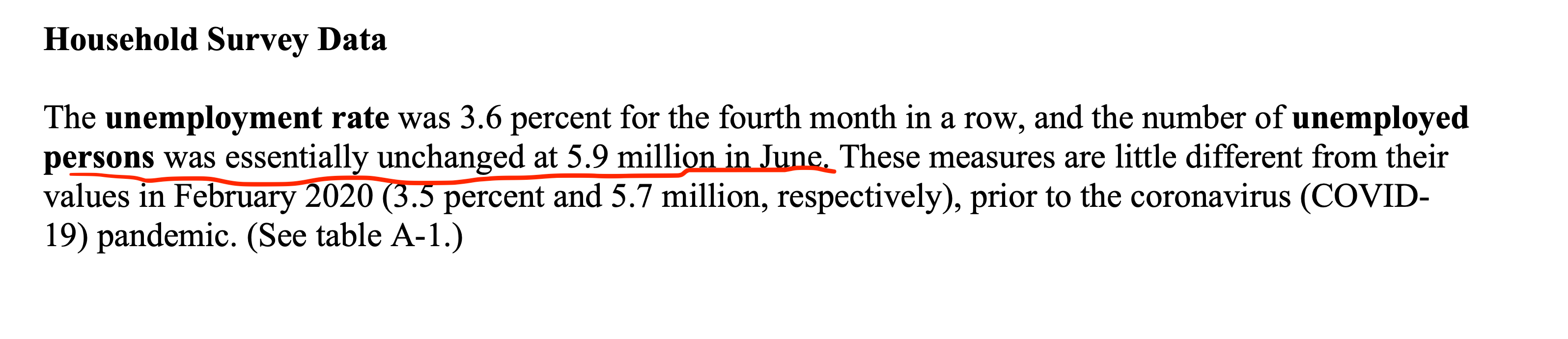

In the first quarter of this year, while we saw a negative GDP number and a slowdown in economic activity, the unemployment rate did not follow the normal path of past recessions. The unemployment rate actually DECLINED from 4% to 3.6%.

This is extremely unusual for a recession.

As the Wall Street Journal stated about current people collecting unemployment:

“At the end of June, 1.3 million Americans were collecting federal unemployment checks, substantially fewer than the 1.7 million people collecting them on average each week during the three years before the pandemic, when the economy was considered to be exceptionally strong. The number of people receiving such benefits topped 6.5 million during the 2007-09 recession and exceeded 3 million during the two earlier downturns.”

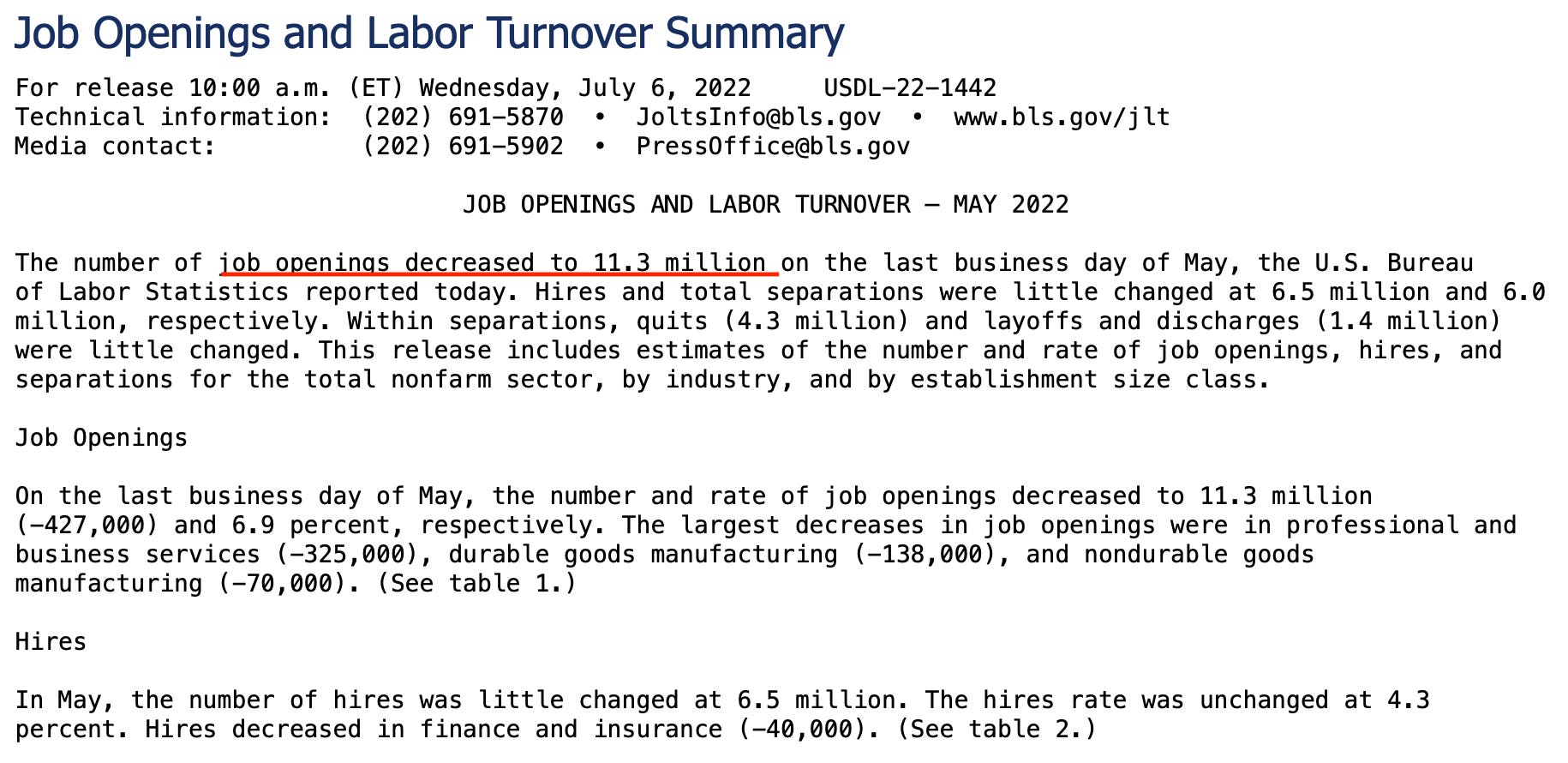

Right now there are more job openings than unemployed.

There are currently 11.3 million job openings in the United States.

While there are only 5.9 million people unemployed.

This means we almost have double the job openings versus unemployed right now in the United States.

If I told this statistic to any economist over the past 100 years, none of them would have predicted we would print a negative GDP number or even mention the big “R” word.

As the Wall Street Journal stated:

“The unemployment rate has increased every time we entered a recession, by as little as 1.9 percentage points in 1960 and 1961 and as much as 11.2 percentage points in 2020. The median increase in the jobless rate among all 12 post-World War II recessions was 3.5 percentage points. The U.S. didn’t escape any of those recessions with a jobless rate below 6.1%.”

The jobless rate today is 3.6%.

So can you have a recession when one of the biggest indicators that go into that calculation currently is the best it has been in mutiple generations?

To answer that question we have to turn to the Eggheads.

The Eggheads Who Forecast Recessions

Bloomberg did a fascinating article on July 12th, 2022 outlining the “Eggheads” who officially say we are in a recession.

Not these British Eggheads

In this article, Bloomberg mentioned a group of eight people, known by Harvard University professor Jeffrey Frankel as “The Ivory Tower Eggheads”, who decide for everyone if we are in fact in a recession or not.

“Recessions have huge impact on markets and US politics. So the NBER Business Cycle Dating Committee of six men and two women -- led by Robert Hall, a 78-year-old Stanford University professor -- can expect harsh criticism if it declines to swiftly declare one on President Joe Biden’s watch following two straight quarters of shrinking GDP.”

This group of eight economist meets in secret, away from any media, and only announces their findings when they feel it’s appropriate. No one knows when they meet, how often they talk, potential motives or incentives of saying we have seen a recession or not.

Because of the large impact their decision may have on politics, businesses, and economic history, this group usually takes about a year, if not longer, to “officially” say we have been in a recession.

This groups definition of a recession is similar to the more detailed definitions we outlined above. Per the article:

Rather than two negative GDP readings, the NBER is looking for a substantial decline in activity over a sustained period of time. The committee sets dates of the peaks of economic activity and troughs based on six monthly data series, including nonfarm payrolls, personal consumption spending and industrial production.

One of the indicators outlined again here is employment.

What will happen if we get to the first quarter of 2023 and continue to see consumption and industrial production weaken but employment stay relatively strong.

Will the eggheads say we are in a recession or not?

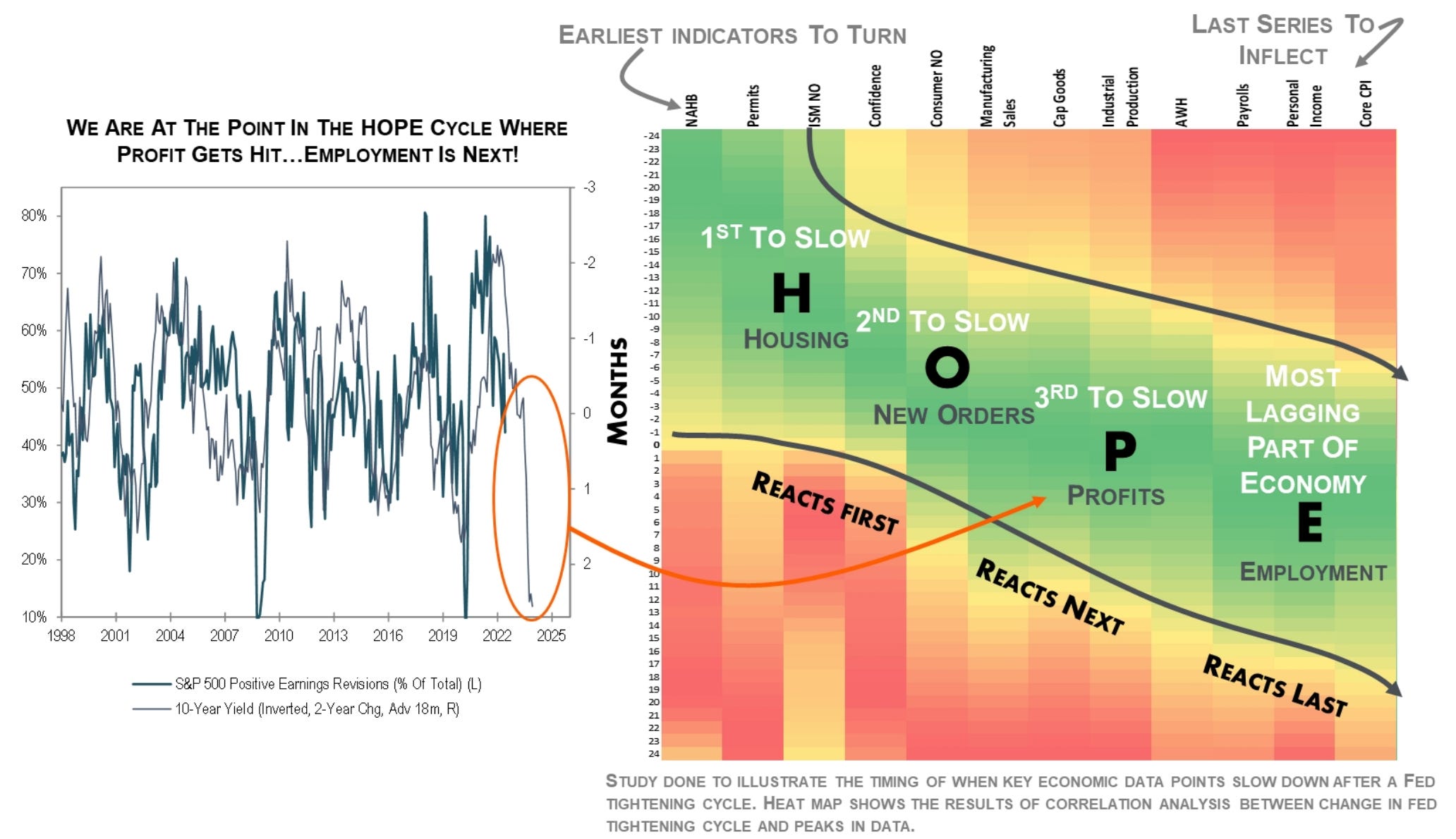

The Economic Cycle of HOPE

To give us some insight into this, Michael Kantrowitz, CFA at Piper Sandler has put together a great graphic outlining how a “normal” economic cycle may proceed.

He calls it the cycle of HOPE.

For Michael, his HOPE outline is playing out as planned.

We saw a significant contraction in June housing data (except for housing prices which continue to be at all-time highs).

Today we saw PMI data which showed a big slowdown, especially in new orders.

And over the last few weeks, many companies reporting their second quarter earnings have missed or guided lower moving forward.

If we use Michael’s outline above as our guide, we should start to see a significant change in the employment market over the next three to six months.

Per his research, employment has always been a lagging indicator (think last on etc move or be inpacted), as the three big levers before it lead to the final outcome of employment slowdown and lay-offs.

Even if we see the employment market weaken from here, we have never been this far into a slowdown and still have 5.1 MILLION more job openings than people to fill those openings.

For us too potentially see a “normal” recession, we will need a bigger slowdown from here in housing, consumer spending, company new orders, and profitability along with a significant tick up in unemployment.

If we do eventually get to the point of a “normal” recession, which the Wall Street journal above stated has never had unemployment below 6.1% (can see past levels in the graphic below), then the next six to twelve months will get very ugly for the jobs market.

First, we would need to see the 11 million jobs opening currently not filled go away. Then to see a 6.1% unemployment rate at a minimum (most economist not predicting this), we will need to see about 10 million people unemployed in the US, up from 5.9 million today.

That is over 15 million job openings and/or currently employed jobs going away. As a comparison, during 2020 we lost slightly over 10 million jobs.

No matter how you slice or dice this data, this would be a huge change in the jobs market and have a big impact on you, your family, and your friends.

Final Thoughts

Will we see a recession in the next six to twelve months?

Right now almost 40% of economist think we will.

It comes down to this:

Will the strong employment market keep us out of a recession, or will it succumb to the weaker economic conditions we will be facing.

As I discussed last week (HERE) about employment, inflation, and the dollar, the Federal Reserve will have a lot to do with how this plays out.

When we get to a situation of a 5% unemployment rate and a 5% inflation rate, which trend will the fed look to fight. Will they want to get inflation lower by continuing to raise rates, or pause rate hikes to keep employment strong and have us deal with elevated inflation for longer.

These two scenarios have both played out in the past.

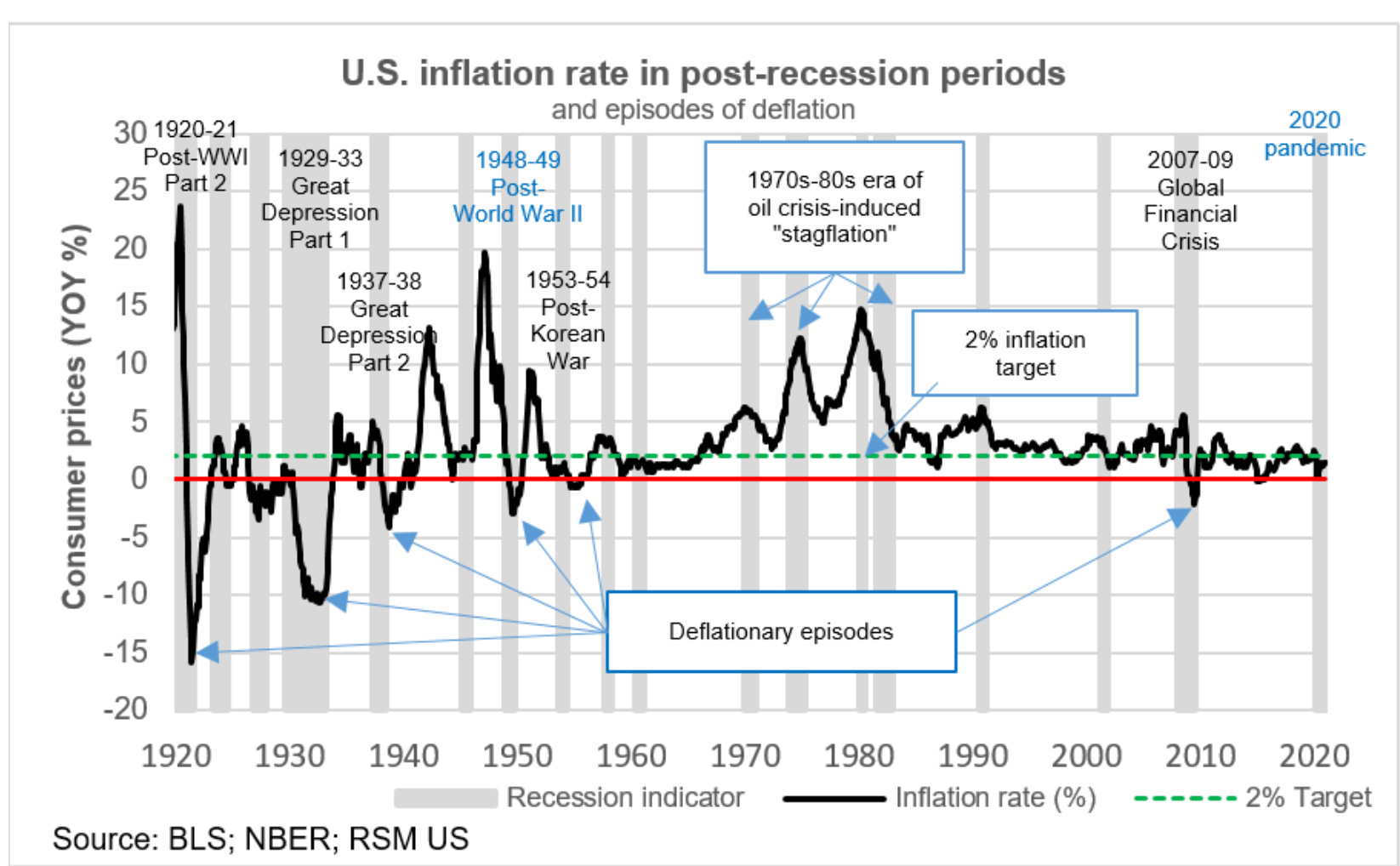

In the 1930’s we had an ultra aggressive Federal Reserve, who helped push inflation back to negative levels right when the economy was trying to get back on track after the great depression, as you can see below. This continued the pain of the Great Depression and ultimately brought on World War II.

On the other side is the weak acting fed of the 1970’s. They focused on employment and not on inflation. Anytime inflation moved lower, they became accommodative to spur growth. But as you can see above, every time the economy started to get better, inflation got worse. Not until a new Fed chart in Volker, which I talked about in detail (HERE)took the lead did we see inflation finally move and stay lower. But to do that, we had to go through some very sever economic pain.

How this plays out no one knows. My guess is we will be more like the 1970’s then the 1930’s or early 1980’s. Once employment weakens and inflation moves lower, I feel the fed will stop, making everyone feel good in the short-term but set us up for the long-term pain from continued rising inflation.

Only time will tell.

Have a wonderful weekend. We will talk next week.

https://marketbusinessnews.com/financial-glossary/recession/

https://www.forbes.com/advisor/investing/what-is-a-recession/

https://www.wsj.com/articles/recession-economy-unemployment-jobs-11656947596

https://www.bloomberg.com/news/articles/2022-07-14/is-the-us-in-a-recession-how-to-prepare-for-economic-downturn

https://www.bloomberg.com/news/newsletters/2022-07-13/what-s-happening-in-the-world-economy-meet-the-eggheads-who-declare-recessions

https://www.bloomberg.com/news/articles/2022-07-12/no-us-recession-until-obscure-panel-of-eggheads-says-it-is-so

Piper Sandler Macro Research July 18, 2022 “HOPE Update” by Michael Kantrowitz, CFA

https://awealthofcommonsense.com/2019/07/the-upside-of-a-recession/

LEGAL STUFF

This commentary is for informational purposes only. This material is not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Enlightened Amadan or its author or the authors employer. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author and not of his current employer. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer. Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made with respect to the accuracy, completeness or timeliness of such information. This information may be subject to change without notice. Enlightened Amadan and its author shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not take into account the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.© 2022 Enlightened Amadan