Brief History of the Federal Reserve (Crappy Title but Very Important Subject to Understand Today)

Brief History of the Federal Reserve (Crappy Title but Very Important Subject to Understand Today)

Economic Perspective of the Week - Week 24, 2022

(12-minute reading time)

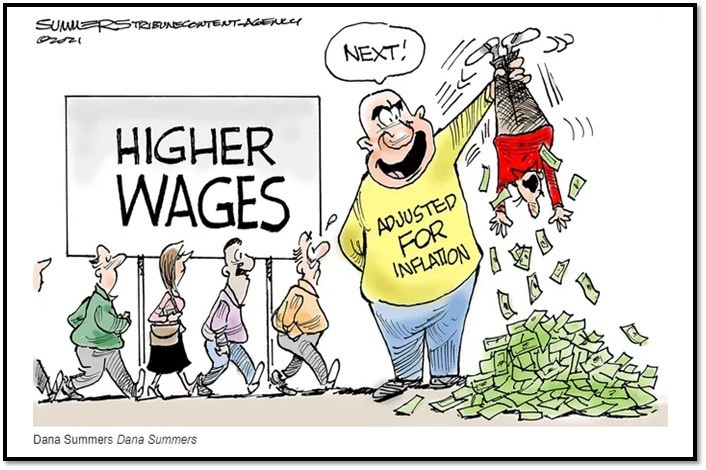

Cartoon of the Week:

Quotes of the Week:

“Comparing this bear market to March 2020 does not make any sense. This is a systemic-based bear market with 9% inflation and a Fed forcing us into a recession. The 2022 bear market combines parts of 2001 and 2008. The government won’t be printing $4 TRILLION this time around.” - The Kobeissi Letter (twitter)

“The Average bear market lasts 289 days and falls 33%. (as of end of May) we just had our 97th trading day of 2022 and the S&P 500 is down 17%. We could have over 200 days left in this bear market. Relief bounces like today (May 23rd, 2022) are crucial and healthy, no -289-day decline moves in a straight line.” - The Kobeissi Letter on Twitter May 23rd, 2022

“When rates go up, things blow up.” - Wall Street Saying

The year was 1977. Yours truly was just entering the world.

The first Star Wars was in movie theaters shattering records.

The first Apple II computer went on sale.

The King died at a very young age of 42.

And the US economy was one filled with mixed emotions of fear, anxiety, and hope.

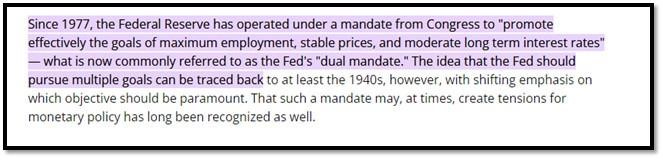

Congress just passed the Federal Reserve Reform Act which mandated “effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

In basic terms, it gave the Federal Reserve a double mandate to control price inflation while at the same time keeping the economy as close to maximum employment WITHOUT firing up inflation.

This new ruling became known as the Feral Reserves “Dual Mandate”.

To understand why this was passed in 1977, we need to look at the issues the US economy went through in the prior 5-years.

The 1970’s Economy (side note: it is Eerily Similar to Today)….

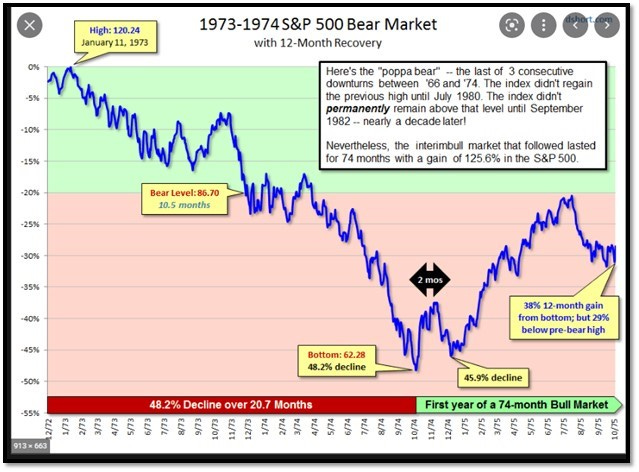

Investors experienced the second-longest bear market in history in 1973-1974 (only the Great Depression was worse).

Unlike other stock market downturns that usually see a sharp crash (think what we saw in 2020), the 1973-1974 bear market was a gradual slide lower amid rising inflation and slowing growth (sound familiar?).

The OPEC oil embargo of October 1973 hit oil prices (let’s sub this for the Russian invasion of Ukraine in 2022) and the Watergate scandal that led to President Nixon's resignation in August 1974 accelerated the declines (again similar to the January 6th investigation going on today).

As stated in the capitalgroup.com snapshot of the 1973-1974 bear market:

“The long grind downward stoked investor pessimism about when stock prices might ever recover.”

In 1973, inflation doubled from 3.3% to 6.3%. (today inflation is up 60% YOY with an 8.6% reading in May 2022 from a 5.4% reading in June 2021) and the S&P 500 that year was down 14.8% as inflation started to take hold from the OPEC oil embargo (as of right now the S&P 500 is down 22% YTD).

In 1974 inflation hit 11%, unemployment moved from 4.9% to 5.6% and the S&P 500 followed its losing year in 1973 with another very ugly return in 1974 of down 26.4%.

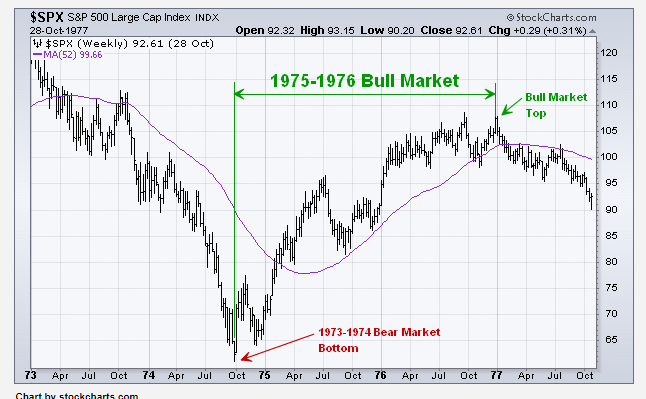

In 1975 inflation gradually moved lower to 9.1% and economic growth was flat on the year. The market had a nice rally of 37% in the hope the worst was behind it.

This trend continued into 1976 and 1977 with inflation continuing to move lower, growth moving higher, and the market showing a nice rebound.

The market thought it was in the clear and congress wanted to make sure we never had to deal with something like the last 5-years ever again.

In 1977 inflation again started to move higher.

With both unemployment and inflation moving higher at the same time, Congress was giving the Federal Reserve the power to do whatever it takes to fight this trend.

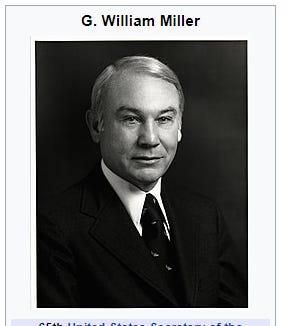

With the new administration, William Miller was introduced as the new Fed Chair in March 1978.

He was inheriting a high inflationary economy that was still suffering from the oil price increase by OPEC. In his first speech, he identified inflation as the nation’s primary domestic challenge.

But even with this viewpoint on inflation, he did not favor aggressive interest rate actions that would jeopardize growth and eventually impact employment.

As a result of his timid approach, inflation put its firm grip on the economy.

People’s habits started to change.

When receiving their paycheck, they spent it right away, knowing prices would be higher tomorrow.

People only spent money on the essentials and did not have any leftover for discretionary spending (read last month’s Target’s and Walmart’s earnings release for similar spending habits today).

While things were looking better in 1977, everyone felt the ugly inflation boogy man right around the corner.

The only way to protect themselves was to spend what they had right away on essentials that they needed before prices potentially moved higher.

This is what inflation does. It changes your spending habits. As the confidence in the currency fades, you quickly sell your money in exchange for tangible goods.

It becomes a vicious cycle. Everyone spends all they have, saving nothing. As a result, there is a shortage of goods. The shortage of goods pushes prices higher and forces you to ask for a pay raise. You get a pay raise and look to spend more on goods, continuing the trend.

This cycle when taken to extremes creates unstable daily conditions.

During the German Hyperinflation market of 1923 known as the “Weimar Republic”, which eventually led to the rise of Hitler, restaurants stopped printing menus because by the time food arrived prices had gone up.

If you lived in 1923 Germany, if you went out to dinner, you would pay for your meal when you sat down, knowing that it would cost more by the time you finished eating.

The picture below is what it cost to buy a loaf of bread in 1923 Germany.

Once inflation takes hold and changes consumer habits, it is extremely difficult to stop.

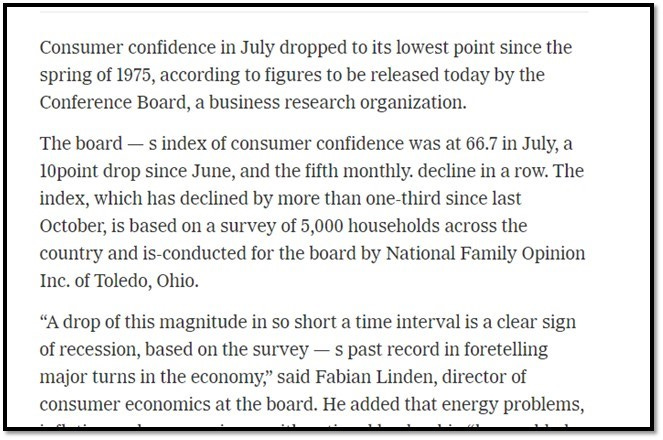

While the markets rallied from 1978 to 1980 under William Miller, by 1979 inflation had again doubled to 11.3%, employment was persistently high, and US consumer confidence was shattered.

The US household was extremely pissed off (similar to today with the Biden administration approval ratings plummeting to new lows).

This headline from the New York Times in 1979 below seems like it could have been written today.

The US consumer was sick of inflation. They saw no hope for the future and as a result, wanted change.

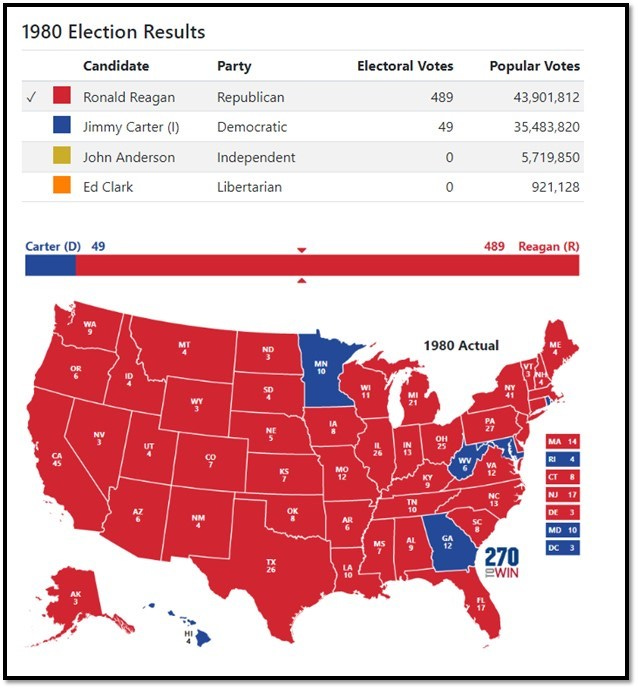

By the time the 1980 election came about, everyone wanted something different, even if that something was an old Western actor from California.

Look at the electoral map from Ronald Reagan’s win in 1980.

This is the definition of a butt-whippin….

Looking at Miller’s time at the Fed, most historians look at it as unsuccessful. While he tried to juggle the dual mandate passed by congress in 1977, clearly the American public was focused on only one mandate, that of inflation.

To understand what the 1970s were like, look no further than what my current boss said about her old boss when she started.

“He used to tell stories about the decade where literally no investor made any money. He managed people’s money for over 10 years and they did not make a dime.”

Enter Paul Volcker

While Paul Volcker is known as Ronald Reagans Fed Chair, he was actually nominated by President Jimmy Carter on July 25, 1979, and took office in August 1979.

When Mr. Volcker took office, the economy was hurting with inflation emerging as the economic and political challenge of the day.

US inflation was out of control. By March 1980 inflation hit 14.8%.

While Mr. Volcker knew he had a dual mandate to keep employment and inflation low, he focused on inflation at the expense of employment.

Mr. Volcker knew the only way to bring down inflation was to put the US economy into a recession.

As a result, from 1979’s interest rate of 11.2%, he raised rates to a Fed Prime rate of 21.5% by December 1980.

This led to the 1980-1982 recession which pushed unemployment to over 10% and saw huge protests around the country by people wanting Volcker’s head.

As Harry Truman wisely stated:

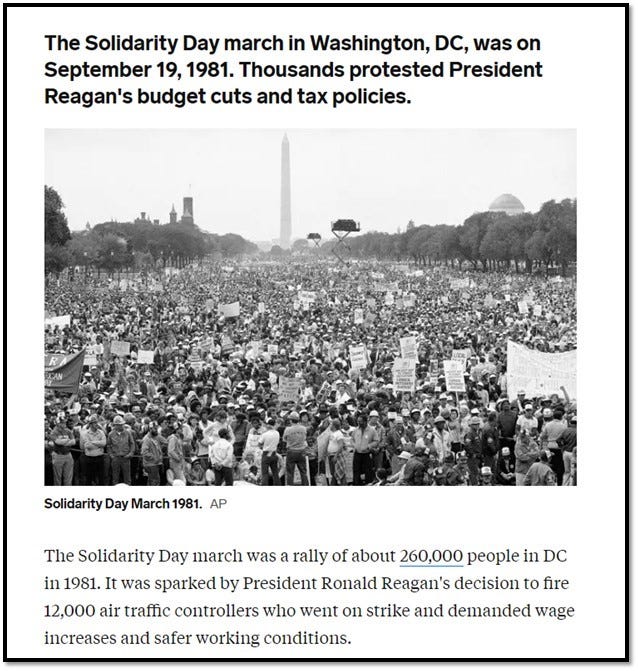

If the population was upset in 1979-1980, by 1981 people were irate and furious.

We saw one of the biggest protest marches in history on Washington DC in 1981.

Ultimately, Mr. Volcker’s plan worked. By 1983 inflation was down to just 3%!!!

Today, Paul Volker is admired by all in the economic community while William Miller is viewed as a total failure.

People today admire both Paul Volker and Ronald Reagan because, despite the death threats, assassination attempts, the protests, and the overall daily barrage of negative press, they stuck to their guns.

Today it is easy to look back and say they made the right decision, but in the middle of the rage, right or wrong, they had a plan to ultimately end inflation and generate economic growth and they stuck to that plan.

I highly doubt any political figure today would have the gumption, balls, and/or persistence to see this through.

Fast Forward to Today

The duel mandate still is alive and well.

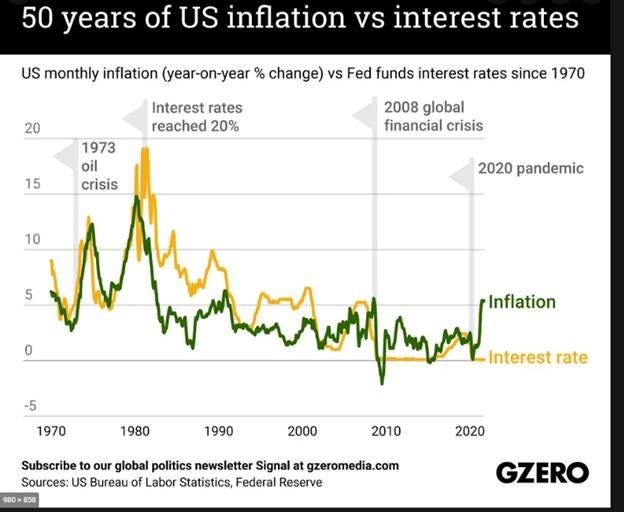

And what we have seen since the 1970s has been a steady decline in inflation (green line chart above).

Due to the rise of globalization since the 1970s, which saw world exports increase 33-fold, the US and other Western countries benefitted from importing deflation.

Instead of the factory worker in Massachusetts making the shirt you are wearing for $15 per hour while working 40 hours per week, we now receive shirts from China and other countries where the same worker makes $1 per day and works 100 hours per week.

This is importing deflation. By us exploiting cheaper overseas workers, we were able to buy goods for cheaper prices.

And because inflation was capped due to globalization, the Federal Reserve saw its mandate as only one thing – to get growth as high as possible and employment as low as possible.

This has led to a very accommodative Federal Reserve since the 1980s and economic booms and busts since then.

From the 1980s bull market run to the 1990 recession which led to the largest market bull run in history in the 1990s to the tech wreck in 2000…which led to a larger fed policy that pushed money into housing only to see a housing market collapse in 2008. This led to the most aggressive fed actions to date, pushing the stock market, the housing market, crypto market, and now commodities markets to unsustainable “bubble” levels.

This is all because of our ability to import deflation while at the same time printing unlimited about of fiat currency without any real negative consequences.

But this time is different. We now stand at a crossroads!!!

The chickens have come home to roost.

Everything we have experienced over the last 40 years is reversing…..

Reversing now….In real-time…..

This is the biggest shift the world has faced in over 40 years!!!

Globalization is now reversing.

China is emerging as a contender to take on the US world order.

And countries are picking sides.

History books will remember this time by two key events that solidified this change.

The first was the COVID pandemic which created supply-chain issues and the other was the invasion of Ukraine by Russia.

The supply chain shortages from COVID have left us vulnerable.

As Warren Buffett stated, we have been shown to be swimming naked.

As a result, we should expect a huge push by companies and our government to nearshoring or make goods and services inside or close to our own borders.

Nearshoring will solve the supply-chain shortages over the intermediate-term, but will also push up prices.

The invasion of Ukraine has forced countries to take sides. Sanctions on Russian Oil started by the US have clearly seen the lines drawn.

The future lines of the coming economic battle.

This new economic and globalization reality has one big impact on all of us.

Instead of importing deflation, we will now be importing inflation.

And as for the Federal Reserve.

Well, I think they did their job when it comes to employment but at a huge cost.

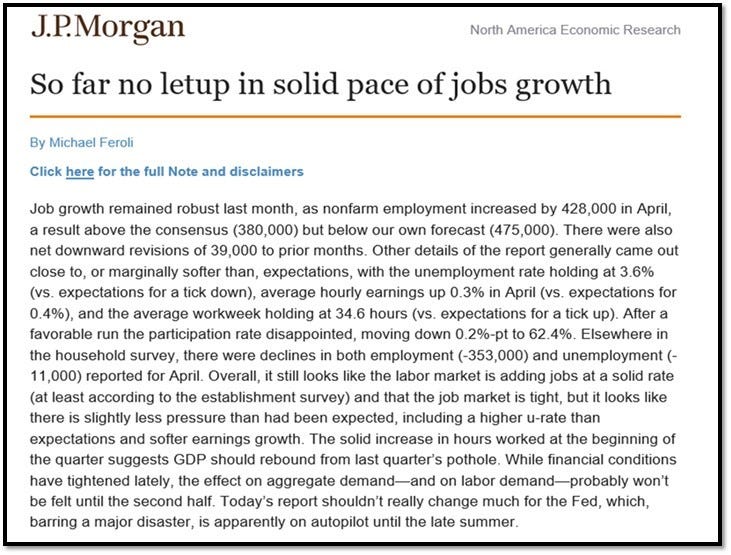

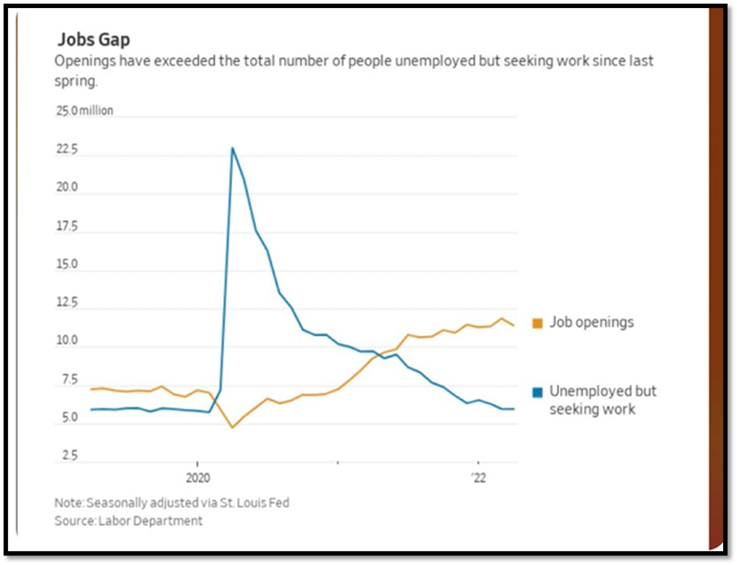

We now have an economy with the strongest jobs market in two generations.

We now have more job openings in our country than unemployed people.

Despite these fantastic stats, the Federal Reserve continued its emergency measures like we were still in 2008.

Think about this for a moment.

The Federal Reserve has a dual mandate stipulated by Congress passed in 1977. Their job was to bring employment lower AND keep prices stable (IE no inflation). As we entered 2022, inflation was moving higher, employment was at a 60-year low, and we still had measures in place like zero interest rate policy and quantiatative easing which pumped money into the market at record levels!!!! These are the same policies we put in place in 2008 when we were 2-3 days away from the entire system blowing up. The market became addicted, the government elect officials became addicted, and the Federal Reserve fell asleep driving drunk going 125 MPH down the economic road. Now we are close to crashing and the driver has finally woken up, but it may be too late.

With the combination of global supply-chain issues, a world energy and food shortage, and a domestic market where anyone can leave their job today and find a higher-paying job elsewhere, we are seeing inflation take hold just like in the mid-1970s.

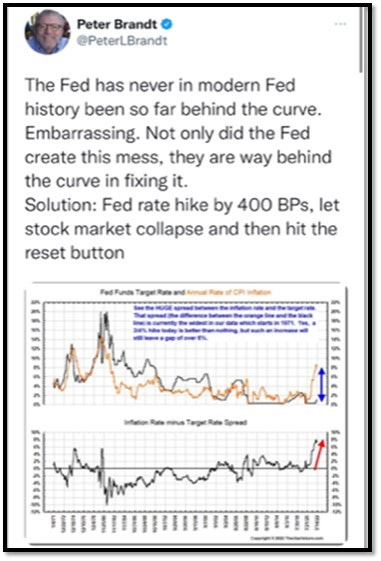

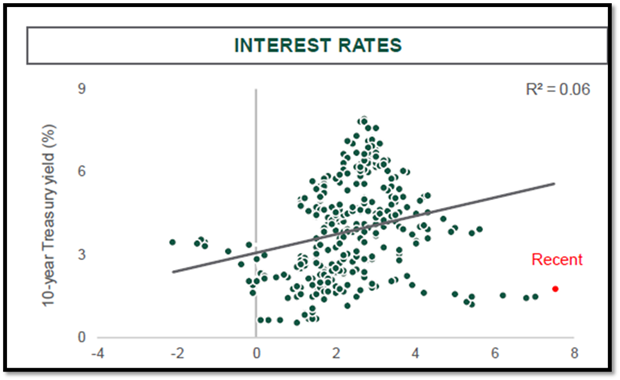

Peter Brandt, the famous trader on Wall Street, said it best.

What does he mean by “behind the curve.”

Look at the chart below. The horizontal line is inflation, the vertical line is 10-year interest rates. You can see historical areas between these two and where we are today.

The curve we are behind is the gray line….We have a long way to go.

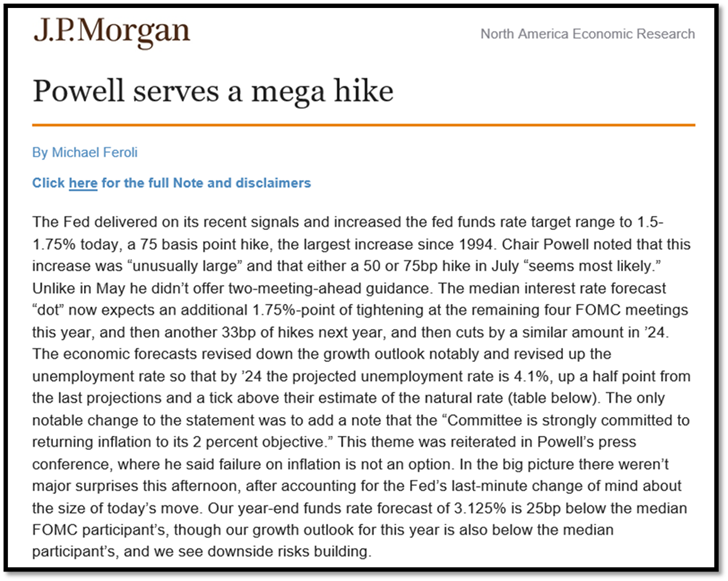

And this is why, despite saying we would not see rate increases over 50 basis points only two months ago, the Federal Reserve this week raise rates by 75 basis points!!!

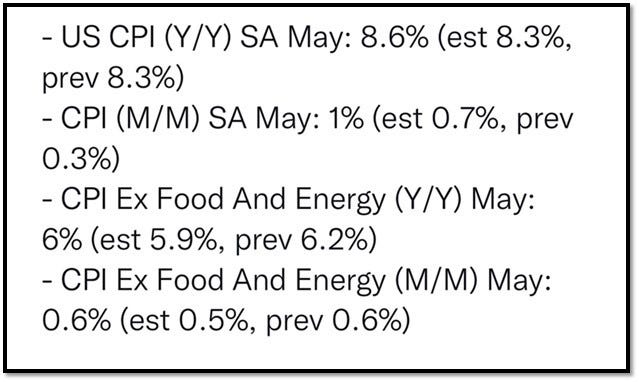

This came after the latest inflation number again came in above expectations.

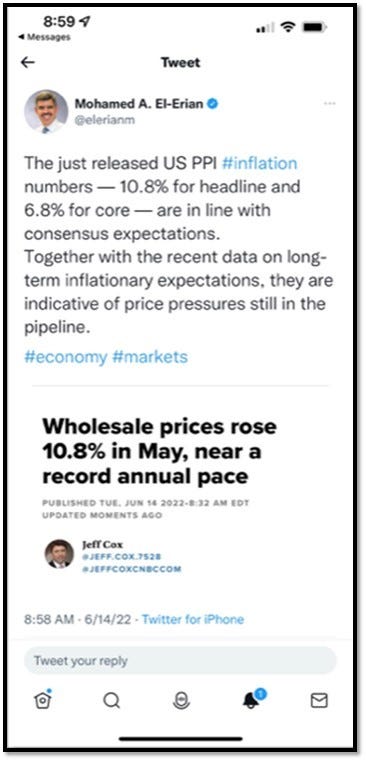

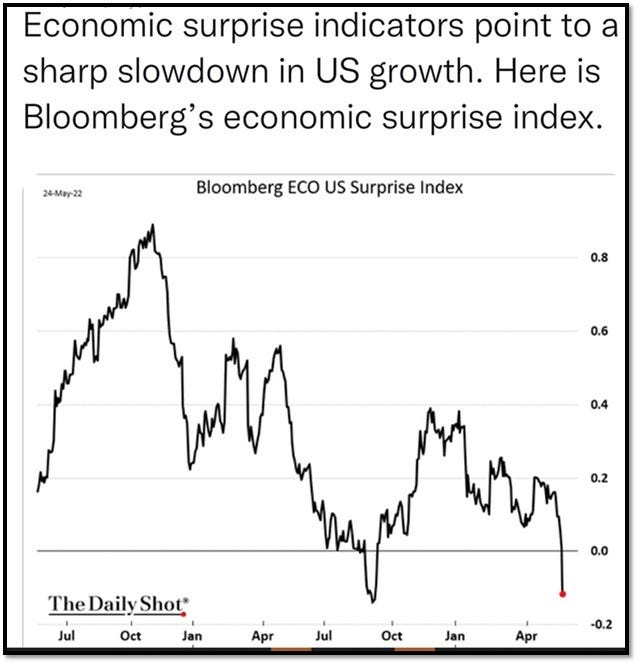

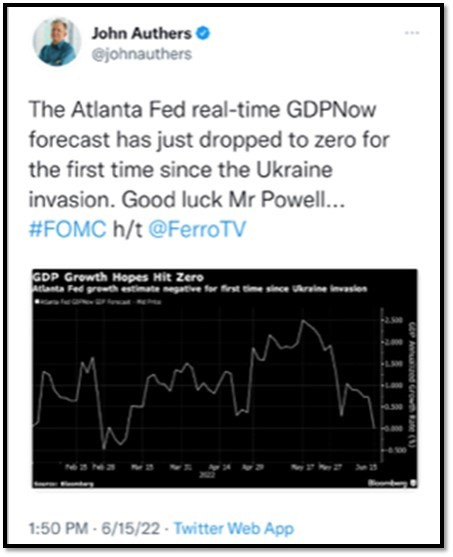

Followed by another ugly inflation indicator.

Which has led to a very fast slowdown in our economy.

And showing us real-time GDP, or growth in the US is basically zero today.

Let me be perfectly clear…This is very important to understand

Since the early 1980s, anytime we have seen these kinds of leading indicators moving this fast to the downside, we have seen a Federal Reserve come to the rescue by cutting rates and injecting liquidity into the market.

Do not expect the Fed to come to our rescue this time around.

Our current Fed Chair Jerome Powell knows history.

He knows and fully understands how the world views Paul Volker with acclaim while viewing William Miller with disdain.

He is focused on one thing and one thing only. Get inflation lower as fast as possible no matter what the cost.

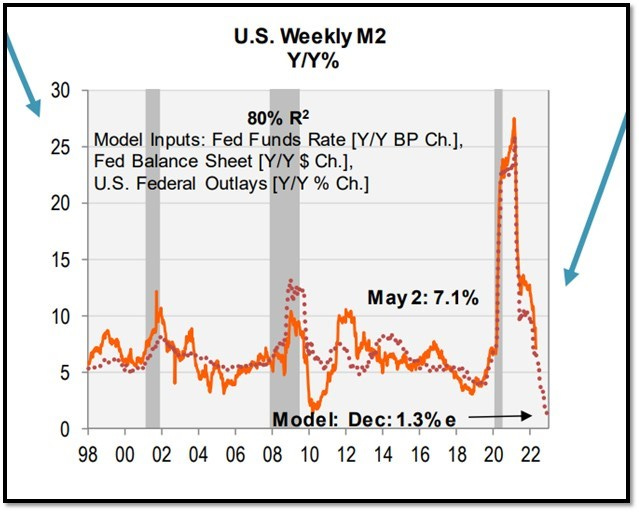

To do this the fed will withdraw liquidity out of the market.

Right now we see the money supply cratering.

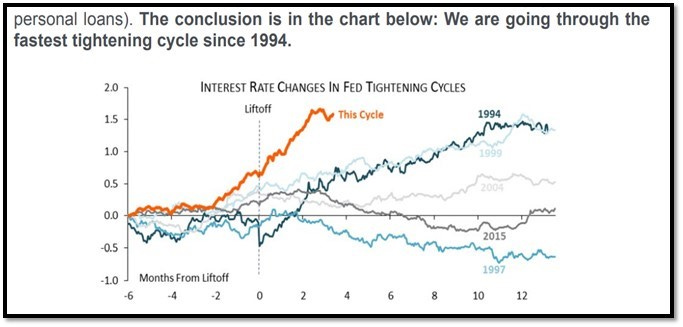

Which will create one of the fastest tightening cycles on record.

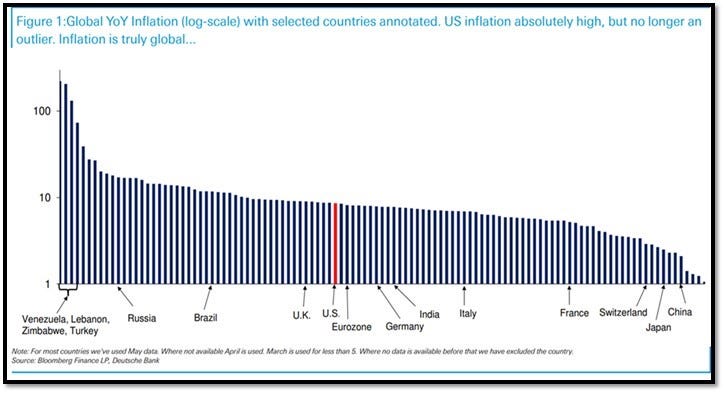

And we are not the only ones. Looking at the chart below, this is the world's central bank problem, and they are all doing the same actions now as the Federal Reserve.

The goal is to bring down the strong employment market without blowing anything up.

This will be a herculean task (there we go again with the metaphors…sorry).

As Bill Dudley, the former President of the New York Fed said in an Opt-ed piece recently:

We have never seen employment rates move higher by more than half a point WITHOUT a full-blown recession.

So while my crystal ball today is very cloudy, I like to use history as my guide (hence the long-winded outline above).

My employer feels we may still see a soft landing. I am in the camp a recession is a done deal.

I am (unlike my firm) also a true believer in the quote from the beginning, “When rates go up, things blow up.” I expect the fed to continue to raise rates aggressively till something blows up. We just have no idea what that something may be.

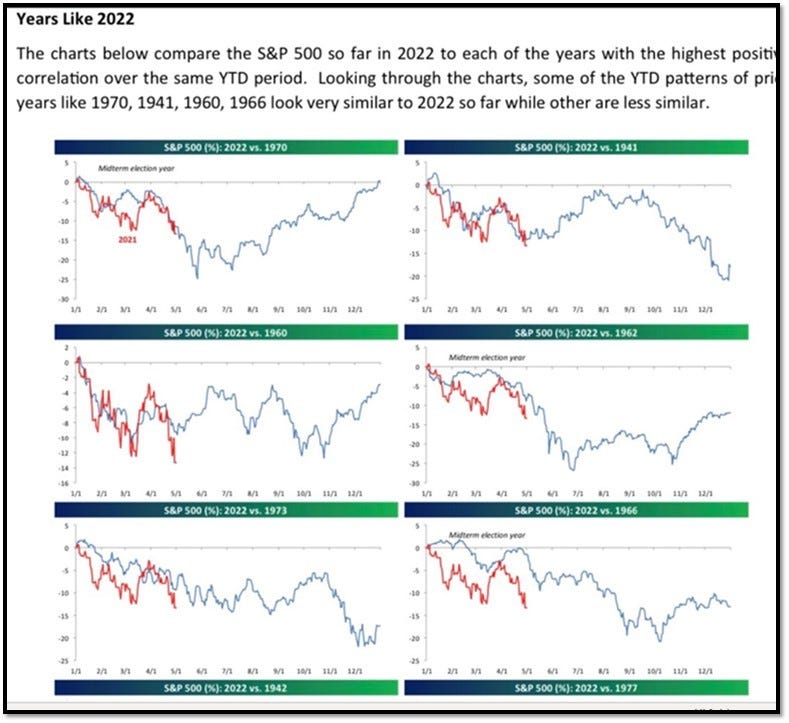

To wrap up, I wanted to share a great chart outlining today’s market action so far YTD and how other markets that started like 2022 ended.

Most seem to go lower from here.

If I was a betting man (again only my view and not that of my employer) I would say the market will rally on any positive news of lower inflation. But similar to the 1941 chart above, this will probably be sold as the impacts from rate hikes start to fully hit the economy.

That is my outlook for the next few months, but where do we go from there and how does this end?

These are the key question everyone should be asking.

Over the next few weeks, I will do my best to try and address these questions.

And sometime in July, I will wrap up this series with a brief history of fiat currency and the potential very long-term ramifications to the thing we call money.

As always, I hope everyone has a wonderful and safe weekend. Please stay cool….Summer is officially here!!!

LEGAL STUFF

This commentary is for informational purposes only. This material is not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Enlightened Amadan or its author or the authors employer. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author and not of his current employer. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made with respect to the accuracy, completeness, or timeliness of such information. This information may be subject to change without notice. Enlightened Amadan and its author shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not consider the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

© 2022 Enlightened Amadan