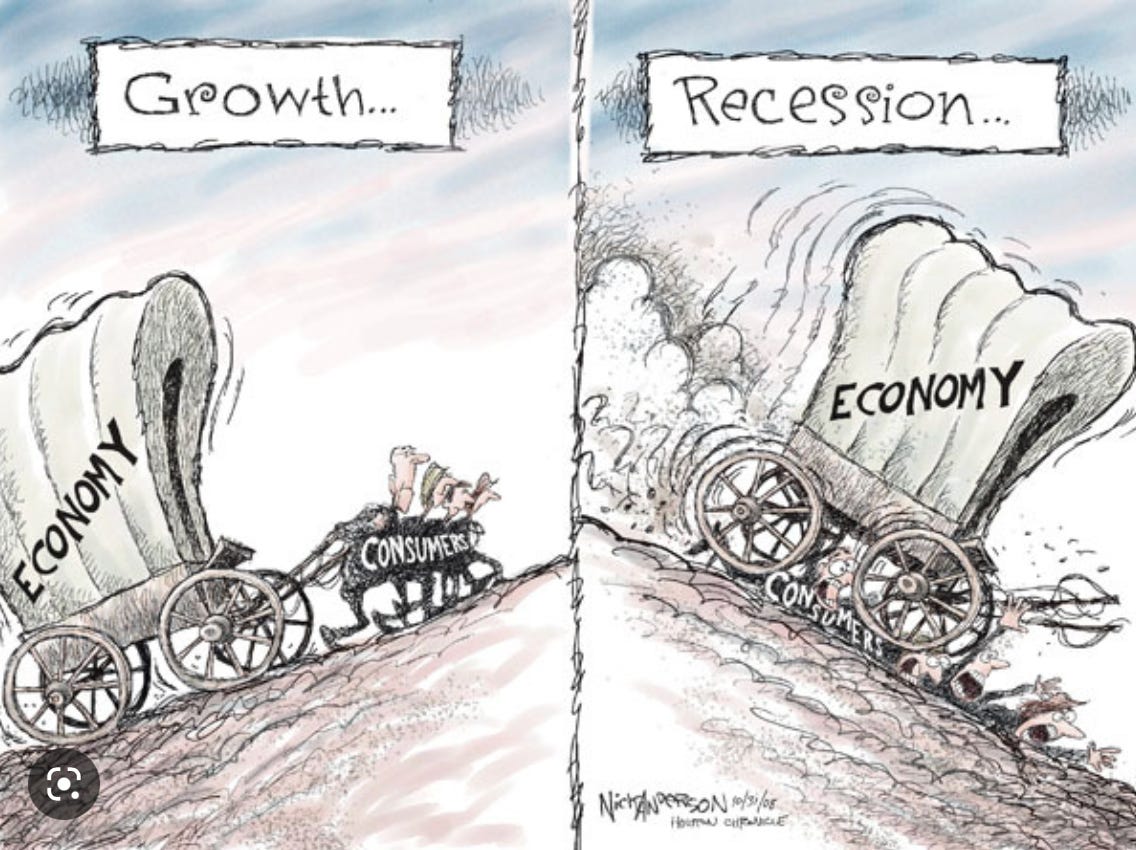

A Race to the Bottom - A Lose-Lose Game of Chicken Between US Consumers and Corporations

A Race to the Bottom - A Lose-Lose Game of Chicken Between US Consumers and Corporations

Corporations have passed on inflationary pressures to the US consumer all year. How long can this last and what does the end game look like?

(10-Minute Read Time)

A QUICK THANK YOU ON THIS SPECIAL DAY

Before I get started today, I wanted to quickly thank all the Veterans out there for your service and sacrifice for our nation.

It is because of you I am able to sit here today and do something I love. To write about the markets, criticize, pass judgments, and give my basic viewpoint with no fear of someone or something coming after me.

Many have given their lives for the greater good of all of us.

Every Veterans Day I pull up the image above and take a moment to reflect. To try to put myself in the shoes of one of those young men in that image. To try to understand the fear, pain, imagery, and ultimate bravery they must have felt to do what they did.

Sometimes as a nation, we get so caught up in the day-to-day BS of politics and forget what these young men in this picture did for all of us. We get so focused on the trees that we forget about the forest. That we are all Americans. Under one flag. The flag stands for freedom and bravery.

Today, please take a moment to reflect. To reflect on the goodness in your life. To reflect on the joy and happiness we all can experience each and every day because of what our current veterans, their fathers, and their forefathers have done for us.

To all you veterans - From the bottom of my heart, THANK YOU!!!!

Cartoon of the Week:

Boy what a day!!!

As Roberto Perli and Benson Durham at Piper Sandler outlined this morning, yesterday’s market action was one for the record books.

Moves like that are why professional investors say never time the market. As you can see below, by missing only a handful of days like yesterday, your overall long-term returns get hit hard.

You have no idea when these types of days will happen. But when they do, they are very healthy for your long-term investment returns.

But why did the market rally so much on Thursday?

After the release of the latest CPI (inflation data) number, we saw the NASDAQ move over 300 points in 30 seconds!!!

This excitement was brought on by a core inflation number month-over-month coming in less than forecast.

What does this mean?

The market changed its thoughts yesterday and is now pricing in peak inflation.

As the chart below shows, if we continue the trend of 0.3% month-over-month or lower, by mid-next year inflation will ONLY be in the 3% range!!!

But don’t get too excited yet (sorry).

As I talked about at the beginning of October HERE, the market was looking for a reason to rally. Bear markets never go straight down. And when you have so much negativity all year, usually the last three months of the year are good for your returns.

There was a ton of built-up energy for a spike higher. It just needed an excuse.

And as I talked about in the second week of October HERE, a “Peak Inflation” narrative is the excuse the market wanted. The market was set up perfectly for a very nice Santa Clause rally.

Why?

Basically, it comes down to this:

lower inflation = fewer rate hikes = less liquidity leaving the market = lower odds of a big recession and/or something blowing up.

But inflation is notoriously sticky.

Just look at the late 1970s as a roadmap.

We saw three separate pullbacks in inflation and rates in the late 1970s. Despite these false alarms, inflation did not peak until a more severe recession 18-24 months after the first shallow recession happened.

I think the discussion of inflation will go away as we enter 2023. Peak inflation is here but that does not mean we are out of the woods.

What will drive the market in 2023 will be one of two things:

1. Corporate earnings weakness

2. US Consumer weakness

Both continue to be resilient, but one of them will crack soon.

Let’s discuss why……

US Corporate Earnings

The market and its “expert” analyst have been predicting an earnings downturn since the beginning of 2022.

We can see this in the number of analyst “downgrades” over the past year.

And using the history of credit standards as our guide, we should have seen a dramatic fall-off in earnings in 2022.

But when we look at profit margin and return on equity (the rate of return a company makes on its investments), they are both sitting at all-time highs.

And as you can see below just looking at margins (% of a dollar you make as profits), we are still well above historical norms.

How can this be?

Well despite the cost pressures businesses are seeing, they have been able to pass these on to you.

Just look at Heinz's (the Ketchup guy’s) latest earning release.

You can see below that while their volumes were down during the year (you are buying less Ketchup from them), they more than offset this weakness with price increases (each ketchup bottle costs more).

The graphic above is provided by Heinz report and the red highlight from Rene Javier Aninao at Corbu

Another great example is from Coca-Cola.

As you can see below, while they had a negative impact from currency (-8% because of the strong dollar) and only 4% volume growth, we saw them offset this with a consolidated price increase of 12% year over year!!!!

Yellow highlight provided by Rene Javier at Corbu from Coca-Cola 3Q 2022 earning report

We are seeing more and more companies passing on their costs to you through price increases.

Let’s look at UPS. Their volumes were down for the quarter but they pushed prices UP by almost 10%!!!

UPS Earnings Release highlights from Corbu Samuel Rines | Managing Director

Another example is from the Sherwin-William Earnings Release:

Margins IMPROVED because of pricing actions.

TRANSLATION:

You Mr. and Mrs. Customer are struggling and we are not seeing the volume of sales we saw in the past. We are also seeing big cost increases in wages and input costs. So what we did was push prices up much higher to cover these cost increases, weaknesses in volumes, and some additional to make extra profits.

You, Mr. and Mrs. consumer, are paying for this inflation. You are paying for OVER 100% of the inflationary pressures in the system. In fact, for most companies, it gives them an excuse to raise prices as much as they can.

But this cannot last forever. Something will have to give.

It’s like a game of chicken. Will the consumer continue to eat all the price increases or will corporations eventually have to give?

The US Consumer

You are feeling the pain.

If you have invested in stocks, bonds, real estate, crypto, or nearly anything this year, you are feeling the pain.

Despite companies pushing all their cost increases onto you, stock prices have still collapsed in 2022.

This is not because of weaker earnings (as we highlighted above), but because of a lower multiple on those earnings.

You see, the market is driven by two inputs.

1. Earnings and the growth of corporate earnings

2. What multiple you pay for those earnings

As you can see below, while earnings have actually gone UP this year (red arrow), the multiple you pay for those earnings have collapsed (blue arrow).

As Joe Weisenthal at Bloomberg so elegantly stated last week:

“Many companies may find themselves in a position where they're able to pass through big price increases and expand margins. But the more companies are able to do this, the more reason the Fed has to be aggressive. And the more aggressive the rate hikes, the more corporate multiples compress. And so to some extent it's whatever the opposite of the paradox of thrift is. We could even call it The Paradox of Greed: When everyone is trying to maximize profits through price increases simultaneously, everyone gets poorer (at least in this current Fed regime, where fighting inflation is the #1 priority).”

While companies are trying to save their behinds by passing on price increases to you, the more they do it the longer the fight against inflation will last.

While companies are feeling the pain, they have been able to pass it on.

This means you as a US consumer are getting hit on all sides.

Not only have you seen your net worth and investments crater this year (chart below) but you are also being forced to pay for all the cost pressures created in the system by inflation.

This double whammy cannot last.

The US consumer was extremely strong coming out of the pandemic but this strength is fading very quickly.

As a recent survey done by JP Morgan stated:

1. During the pandemic, households amassed $2.1 trillion in excess saving, which is dwindling very quickly

2. All income quartiles saw higher real incomes in 2022 vs 2019 with those in the lowest income quartile experiencing the largest relative gains

3. Per a recently JPM survey, 50% of respondence expect to reduce spending on non-essential items by at least 10% in the coming months relative to the start of the year.

All the work done by governments to prop up the consumer (what started this inflation spiral) during the pandemic is now being dwindled away by inflation and corporate profits. Everyone is losing.

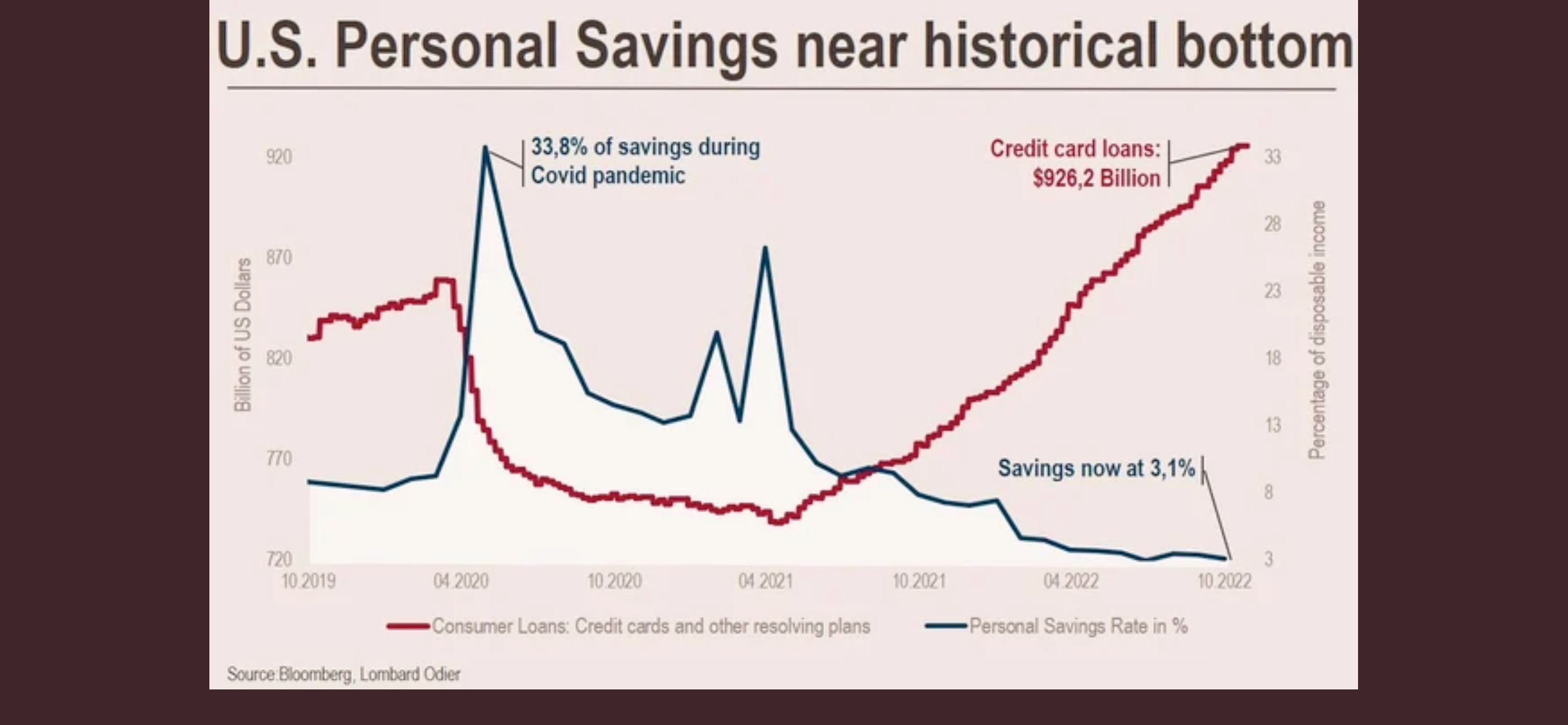

As you can see below, the savings rate of the US consumer (blue line) spiked during the pandemic but quickly faded down to nearly zero.

Below is the same blue line highlighting the saving rate combined with the US consumer credit card loans.

Below is a longer-term view of the same information (the red line is the savings rate and the blue line is credit card balances).

Savings rates have gone to zero while credit card balances have skyrocketed.

This is not sustainable.

And while you may be getting raises from your employers (chart below-showing wages YOY strong and becoming a bigger part of company costs).......

Those raises are not keeping pace with inflation.

When we look at real wages (wage increases - inflation) below, we have not made enough money to keep us ahead of the game.

Which is ultimately pushing the pressure and stress on the US consumer much higher.

This pressure is starting to be seen in things like late auto payments, which have recently spiked higher.

You are starting to change your spending habits.

As you can see below, while last year was focused on not having enough stuff in the system because of supply chain issues, now we are having too MUCH stuff in the system because you are spending less.

When we get too much stuff in the system and corporations can no longer pass on the costs to you, they will start to fire people to save on costs.

This starts the negative feedback loop...

Less spending = more cost cuts = more firings = less spending = recession......

This loop is just beginning. The Fed hopes it can control inflation and lower it before the negative feedback loop begins. I have my doubts.

You, as a consumer, are already starting to crack.

You are already spending less on stuff.

Because your spending habits buying stuff account for almost 70% of our growth, expect some negative growth numbers in 2023 and 2024.

We will get more insight on this trend next week when Walmart, Target, and Home Depot all report their earnings. It will be interesting to see what they have to say about US consumer spending habits.

The REAL Recession is Coming…

While we saw a technical recession in early 2022, everything is lining up now to see an actual recession in 2023 or 2024.

As you can see above, the only thing missing is the initial jobless claims (IE firings).

It’s coming....

So while the Federal Reserve is still forecasting a “soft landing” and the market yesterday priced in a higher percentage of a soft landing, ultimately, we are just starting the negative feedback loop that usually leads to a recession.

(Great reason why we should take the Fed’s forecast with a grain of salt)

Conclusion

I still expect the market to rally into year-end and give us a nice Santa-Clause rally. I would not be surprised if one of the major indexes closed green on the year.

But as Public Enemy once said, Don’t Believe the Hype….

Expect 2023 to bring in its own challenges. These challenges may be more difficult than the inflation challenge of 2022. At least on the economic front.

You are tapped out and are making cutbacks in your day-to-day spending habits. Corporations have drained you of almost everything they can. Eventually, to save themselves, they will start firing you in droves. And when this happens, unemployment will spike higher, which will put more pressure on corporate earnings and spending, which will have us facing a more normalized recession in mid-to-late 2023.

Buckle up......

One more thing before I go.

Last month Stanley Druckenmiller presented his viewpoints on the current market. If there was one person you should listen to in the market (besides me of course :) , it is Mr. Druckenmiller.

Below I have put his main takeaways published on the CNBC website.

To read the article please click HERE

If you want to listen to his entire discussion, please click the video below. It is 25 minutes long but well worth your time.

Have a wonderful weekend!!!

LEGAL STUFF

This commentary is for informational purposes only. This material is not intended to be, nor should they be construed as financial, legal, tax or investment advice and do not constitute an opinion or recommendation by Enlightened Amadan or its author or the authors employer. You should consult appropriate advisors concerning such matters. This material presents information through the date indicated, is only a guide to the author’s current expectations and is subject to revision by the author, though the author is under no obligation to do so. This material may contain commentary on: broad-based indices; economic, political, or market conditions; particular types of securities; and/or technical analysis concerning the demand and supply for a sector, index or industry based on trading volume and price. The views expressed herein are solely those of the author and not of his current employer. This material should not be construed as a recommendation, or advice or an offer or solicitation with respect to the purchase or sale of any investment. The information in this report is not intended to provide a basis on which you could make an investment decision on any particular security or its issuer.

Certain information has been provided by and/or is based on third party sources and, although such information is believed to be reliable, no representation is made with respect to the accuracy, completeness, or timeliness of such information. This information may be subject to change without notice. Enlightened Amadan and its author shall not be liable to any person in any way whatsoever for any losses, costs, or claims for your reliance on this material. Nothing herein is, or shall be relied on as, a promise or representation as to future performance.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Any financial instruments mentioned herein are speculative in nature and may involve risk to principal and interest. Any prices or levels shown are either historical or purely indicative. This material does not consider the particular investment objectives or financial circumstances, objectives or needs of any specific investor, and are not intended as recommendations of particular securities, investment products, or other financial products or strategies to particular clients. Securities, investment products, other financial products or strategies discussed herein may not be suitable for all investors. The recipient of this report must make its own independent decisions regarding any securities, investment products or other financial products mentioned herein.

© 2022 Enlightened Amadan