Why are Gas Prices so High?

Why are Gas Prices so High?

Economic Perspective of the Week - Week 13, 2022 - Energy 101 - Part 2

Cartoon of the Week:

Quote of the Week:

“What’s more given current events, the sanctions that would have the most impact on the barbarism of Putin’s Russia would be to flood the global market with America’s own oil and natural gas, driving prices down and depriving a rogue state of resources to fund an illegitimate war.”

- Jason Trennert Strategas Strategist

Why Are Gas Prices So High?

In October 1773, the US consumer faced a problem. The Arab State members of OPEC (Organization of Petroleum Exporting Countries) declared economic war on the United States in response to our support for Israel in the Yom Kippur War. The members of OPEC decided to cut the supply of oil to the US, creating the gas shortage of the mid-1970s.

This was the first real supply shortage the post-World War 2 U.S. consumer has felt. And it was ugly.

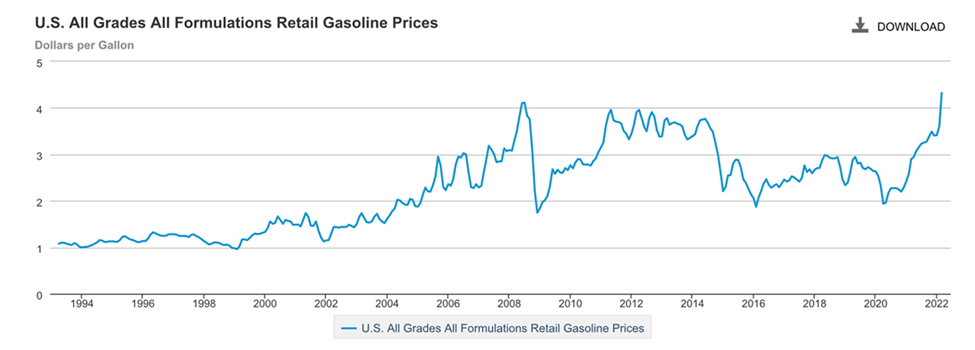

In June 1973, the price of a gallon of gas was under 50 cents. By March 1974, that same gallon of gas spiked to over $4 per gallon.

To ration gas, the government implemented odd and even days. Depending on your license plate last digit was the day you were allowed to fill up your tank of gas.

The government also implemented a lower speed limit on highways to conserve gas.

The 1970s were a very difficult decade economically for most Americans and it was started by the 1973 oil crisis.

The similarities between the 1970s and today are startling. Like the 1960s, the 2010s where a good decade economically but super hostile politically. The 70s saw a rise of inflation like today and that rise was started by a supply issues with oil, similar to today.

But the big difference between then and now on the oil front is instead of it being driven by foreign countries blatantly cutting supply to push up prices like they did in the 70s, today it’s more structural in nature, a COVID hangover, and partially, because of our own doing.

The Law of Supply and Demand

To understand why we are facing rising gas prices today, we need to geek out for 30 seconds and go back to all of our favorite classes from school - economics 101.

Economics is filled with theories and ideas that frankly do not make sense sometimes.

But there is one theory that has stood the test of time. And as a result, it has turned into a law.

The law of supply and demand.

It’s the basic interaction between the sellers of something and the buyers of something.

The core idea is that if demand for an item goes up, the price of that item will move higher.

Think of the Cabbage Patch Kid from the mid-1980s, or the first Nintendo, or Teddy Ruxpin.

Or the shortages today in the new Microsoft Series X Xbox.

All driven by lack of supply.

If you were a kid in the 1980s, the toys above were easy to find during the year but quickly disappeared during the Christmas season. And if you could find them, the price you had to pay was 3-5 times higher.

This was depicted perfectly in the scene from Jingle All the Way Movie, starring the great Arnold.

As this scene depicts, Arnold Schwarzenegger was dealing with the increase in Christmas demand for the Turbo Man action figure, which could not be found in any store (lack of supply).

If eBay was around in 1996, Arnold would probably be able to find one there, but the price would be significantly higher than the sticker price in the store.

When we lack the supply of a good, the prices move up.

When prices move up, the maker of that item makes more money, and with that money invests in making more.

This increases the supply of that product.

But if they supply too much, the price of that product would move lower.

Eventually, over time, supply and demand will automatically balance out, creating what we call an equilibrium price.

All the equilibrium price is basically where a seller supplies and where the buyer’s demands come in line and where both sides are happy.

This one law dominates everything in our lives.

From the money supply to the prices we pay, to the discounts we get, and to the ability for us to have an unlimited amount of products on our shelves.

It is why capitalism works. Capitalism is just the most efficient economic structure to find the equilibrium price of any good in the market.

If there was one thing EVERYONE in the world should know from economics - it’s the law of supply and demand.

Ok Done with school…sorry about that…

Shale Revolution

As I talked about last week HERE about Energy Independence and the introduction of Shale technology in the United States, our oil and gas production spiked in the mid-2010s.

This created an economic boom for jobs in the oil and gas industry.

It also increased the amount of oil SUPPLY here in our country.

If you wanted to make money, you headed to a shale area.

This also created an influx of people sleeping in Walmart parking lots in oil shale-rich areas like Williston, North Dakota.

To keep up with this increase in SUPPLY, we expanded our storage capacity.

This expansion in capacity created the largest oil storage area in the world.

Cushing Oklahoma….

The video below is from Cushing OK, the largest oil storage area in the world!!!

With this storage capacity in Cushing increasing to keep up with increasing SUPPLY, our storage quickly approached capacity.

As a result of all this SUPPLY, the US was quickly becoming an energy powerhouse.

As a result, in 2015 the Obama administration was forced to lift a 40-year old trade restriction outlawing US producers from exporting crude oil and gas.

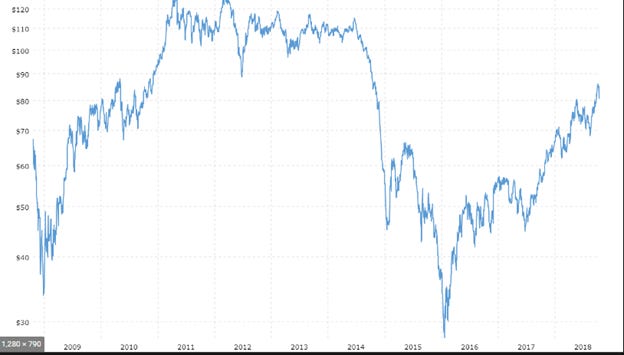

And as our storage continued to fill up, and this new law came into effect, the world price of oil moved lower.

As price moved under $60 a barrel in 2015-2016 because of the new SUPPLY coming online from the US, world SUPPLY in other areas was shutting down because they were no longer profitable.

As you can see below, a number of countries’ production is not profitable at under $60 a barrel.

During this time we saw a significant number of Exploration and Production companies open up.

Banks, hedge funds, and normal investors were willing to give them money.

From about 2010 to 2015, we poured over $600 BILLION into shale production companies.

This amount of money created a dilemma.

To be profitable with a price that is moving lower, what do you have to do?

You guessed it…Drill faster….produce more…and that is what US shale did.

While you were enjoying cheap gas at the pump in 2014-2017, major structural issues were happening in the oil market.

Companies around the world were shutting down projects.

US companies were drilling their best and cheapest wells in hopes to keep pace with the fall in prices.

And the money that was needed for future projects was no longer available.

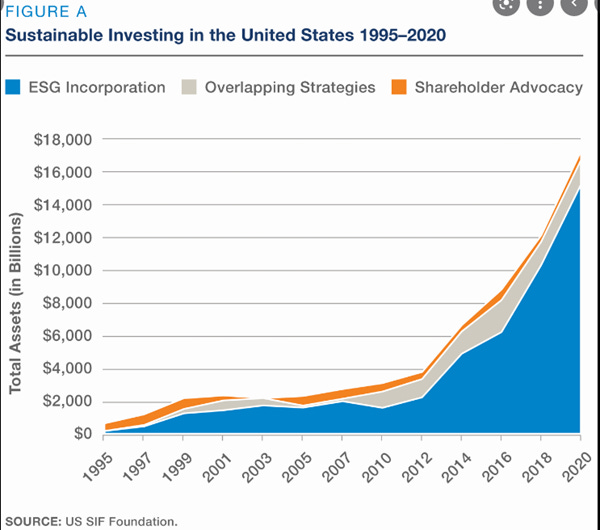

With the combination of lower prices making only the best wells profitable combined with a new focus by investors like yourself on Sustainable Investments, the perfect storm was lining up to impact the oil markets come the start of the 2020s.

JP Morgan Oil team published a detailed note in March 2020 that made the case for the world to see peak oil production in 2022 and to face significantly higher prices in oil and gas as the 2020s progress…

The above chart highlights the significant rise in ESG investing (Environmental, Social, and Governance) which shunned all investments into oil or gas companies.

The writing was on the wall.

Even some of the biggest companies in the world that produce oil looked to change their stripes to get more investors interested.

Enter the COVID Pandemic

COVID created the fastest economic downturn in the history of the world.

In a matter of months, growth went from a normal 2% GDP growth to -6%!!!

As Pierre Andurand, a French hedge fund manager specializing in the oil market said on a recent Odd Lots Podcast:

“The oil market is not built to withstand this type of volatility overnight. Demand collapsed by over 20%. It took only a few months to fill up the storage capacity around the world.”

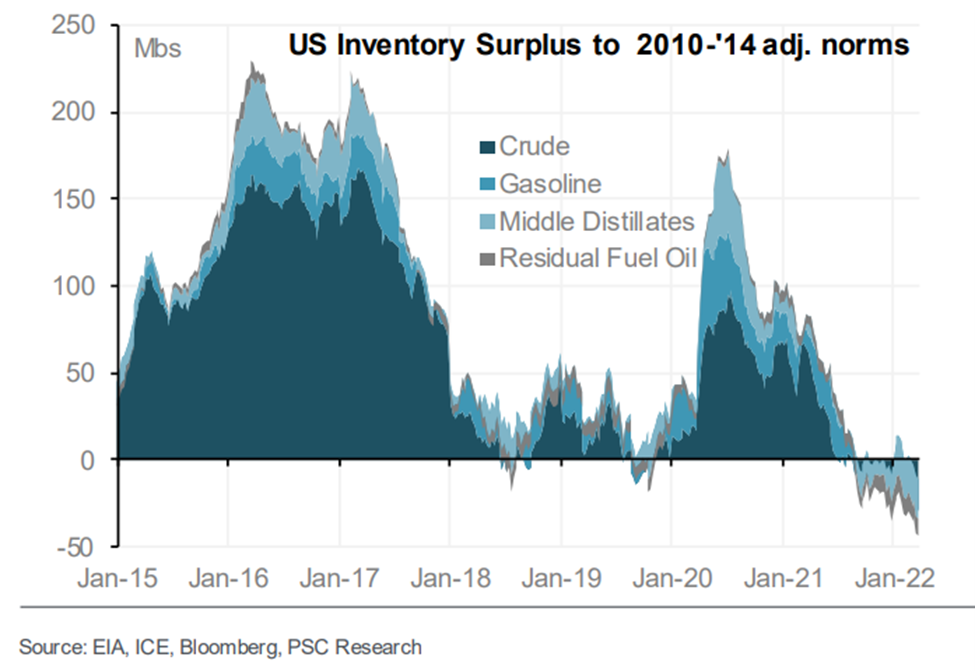

While we did increase storage for oil here in the states, the storage market overall was still small relative to oil production and use.

By 2020, the world had about 100 days of oil storage capacity in total.

Calculation:

Per Rystad Energy, an oil consultant agency, the world has about 9.5 billion barrels of crude and product storage around the world (including tankers).

With demand around the world at about 100 million barrels per day, this means we have about 95 – 100 days of oil storage capacity in the world.

Normal oil use prior to the pandemic was about 100 million barrels per day. This usage dropped by 20% overnight due to COVID.

If our world storage tanks were empty prior to COVID, it would take about 475 days to fill them up completely.

Unfortunately, we were just entering peak storage time of the year (we store more oil prior to summer where the world drives more and needs more oil). As a result, within 2 months of the start of COVID we were at 70-80% of our peak storage capacity.

We were quickly facing a very BIG problem….

Where will we put all our oil…

Enter the Futures Market

Whenever we came close to running out of storage capacity or running out of oil in the past, the futures price of oil would change, creating more DEMAND or less DEMAND by the consumer and controlling SUPPLY coming from the producers.

As Pierre Andurand stated:

“The role of the futures market and speculators is to help make the price of oil move far enough so the tanks are never 100% full or never 100% empty. If this is the case, then oil will fall to zero or could go to $500 or more dollars per barrel. Price needs to move to keep supply and demand is some type of balance.”

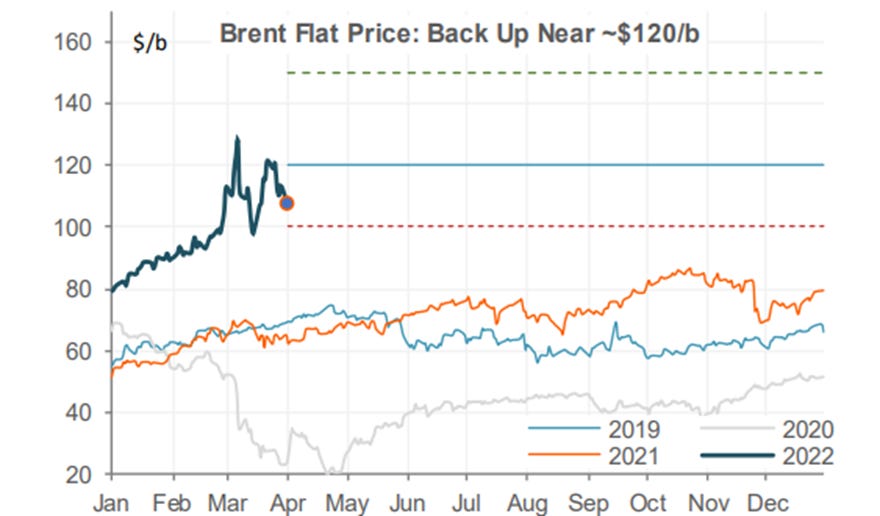

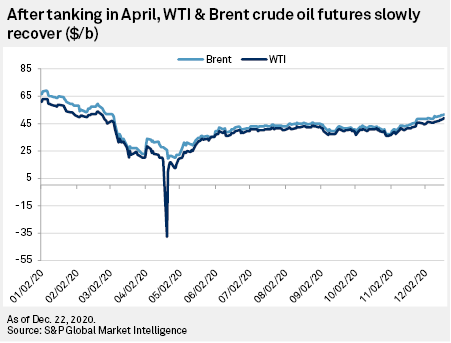

As you can see below, going into March of 2020, oil was already below $60 a barrel.

This was the level where most production around the world would shut down except for the best wells.

(2020 is the light gray line above)

But as these best wells continued to produce in the face of a world shut-down, the futures market quickly tried to adapt.

As you can see above, on the real price of oil, we got near $20 a barrel in May 2020.

But on the futures market, which again is used to try and control SUPPLY and DEMAND, price did something no one would have ever guessed could have happened.

It dropped to NEGATIVE $35 per barrel!!!!

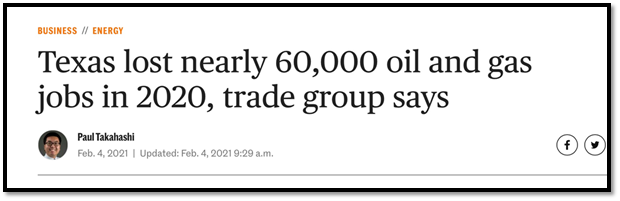

And on this news, companies around the world shut down as fast as possible.

Shale companies here in the US quickly shut down and fired everyone they could.

To Pour Gas on the Fire - Enter Russia

With the introduction of US shale to the world oil market, the Saudis wanted to firm up their grasp on the world energy markets.

The US quickly showed they could be the marginal producer, which gave us the ability to control world prices.

The Saudis did not like this at all….

As a result, they brought Russia into the OPEC grouping and called in OPEC +.

The goal of OPEC is to control the price of oil enough to keep it sustainable and profitable for all to drill and make money. When prices fall too low, they cut SUPPLY and when prices get too high (with the idea it may cause a recession) they increase SUPPLY.

Bringing in Russia gave them more power over a bigger percentage of world oil production.

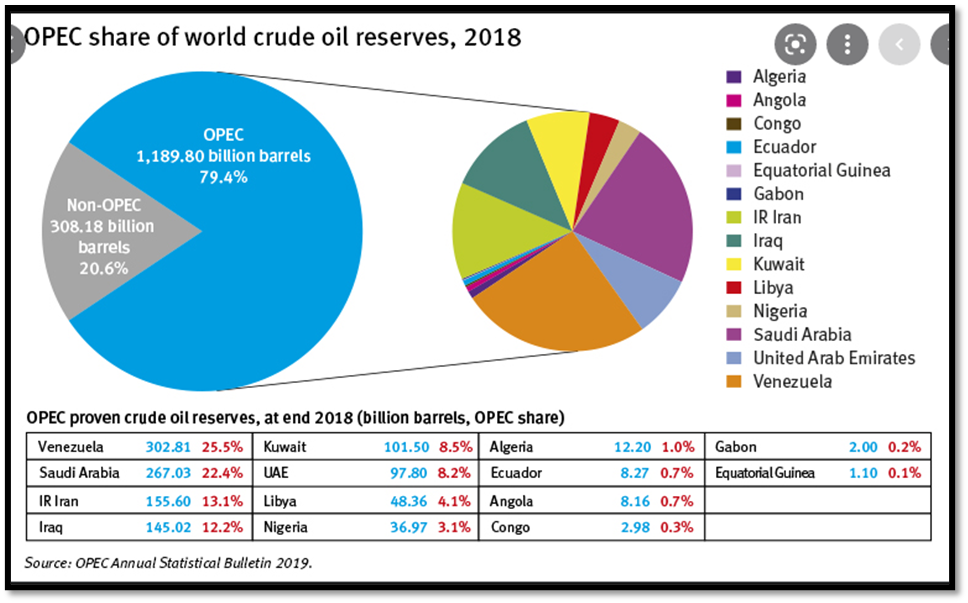

OPEC today controls about 40% of the world's oil production yearly and 80% of world reserves (oil that can be used in the future).

All was going well for OPEC + until 2020 when they agreed to a SUPPLY cut to help support the price of oil during the COVID shut down.

Russia rejected the demand.

As a result, an alleged economic oil SUPPLY war started between Russia and Saudi in the middle of COVID shut down, adding to pricing pressure in the futures market we saw above.

The Saudi and Russian oil war was adding SUPPLY to go into storage right when they should have been cutting SUPPLY.

In April 2020 Reuters reported that:

“If Saudi Arabia failed to rein in its oil SUPPLY, the US senators would call the White House to impose sanctions on Saudi Arabia, pull out all US troops from the kingdom and put high tariffs on Saudi oil.”

On April 9th, Russia and Saudi Arabia agreed to oil production cuts of 10 million barrels per day!!! A record SUPPLY cut announcement.

Current Oil Demand

Looking at our GDP chart again, you can see the dark line below showing GDP growth and forecasted growth.

The orange line is a trend line.

While COVID created the fastest economic contraction on record, the Fed and Central Banks’ stimulus created the fastest economic recovery on record!!!!

You can see even now we are forecasted to grow above trend for the next year if not longer. (dark line above orange line)

With higher growth comes higher DEMAND.

We hit peak oil demand in 2019 of 101.7 million barrels per day.

In early 2022, we are at 100 million barrels per day and because of record economic growth we will hit an all-time peak of 103 million barrels a day of oil DEMAND by this summer.

So now we fact the opposite effect of what we faced in the downturn.

We have the highest DEMAND on record coming this summer but SUPPLY cannot keep up.

When oil production shuts down like it did around the world in 2014-2020, and you have minimal investment into keeping projects running, it takes a while to get things back up and running.

US shale is probably the quickest to come back online.

On average it will take shale companies 12-18 months to get ramped back up.

As you can see below, the number of drilling rigs in deployment usually is a leading indicator of oil production.

And oil rigs in the US shale regions are slowly getting back online.

Which is gradually pushing up production in the United States.

But US producers have already stated they will take their time.

They have lost money, faced many bankruptcies, and lost billions of investors’ dollars over the past 10 years.

Now that they are making money, they do not want to flood the market with new oil right at the time we may face a slowdown economically.

Internationally, it takes much longer to get production up and running again.

In some experts’ opinions, it may take 2 to 7 years to get production ramped back up to peak levels around the world.

So while Biden today announced the release of 1 million barrels per day (this is equal to what Iran could produce if we took off the sanctions), this will probably have little impact over the long term.

Rising gas prices are a politician’s worst nightmare.

Biden and his administration had to do something, as everyone votes by way of the pump.

But as we outlined, this is a structural issue that took years in the making.

This issue would be happening today to whoever was in office.

BUT

The Biden administration has made no friends in the oil and gas business by sending the wrong message to the industry at the beginning of his administration with Keystone and Public Land Leases.

(which by the way neither of these changes impacted our situation today at all)

Instead of parading the Oil and Gas leaders through congress, why not sit down with them and layout a plan for how we can quickly ramp up capacity and

maybe guarantee their debt financing on new production (will never happen but just my idea).

There will be no quick solution.

Prices will gradually move higher as DEMAND moves higher.

As a world, at least in the short-term, it seems like our SUPPLY is tapped.

And with both Iran and Russia now off the market, SUPPLY has just become more difficult to keep pace with DEMAND.

And as we said at the beginning, just like Teddy Ruxpin or Turbo Man, when demand outstrips SUPPLY, prices have to go up or you run out of SUPPLY.

We will not have shale production as we had in 2008-2015 to fight higher prices.

We may be in for a long “Super Cycle” of high energy prices for years to come just like JP Morgan laid out in 2018 and 2020.

Let’s just hope it does not get as worse as it did in the 1970s. To be as bad as it was in the 1970s, the cost of a gallon of gas would need to go above $16 per gallon.

So when your dad tells you the story about their gas and oil issues back in the day, he was in fact correct. It was much worse.

Next week we will talk about refining and why we import oil despite the fact we could be us “energy Independent” as it relates to oil.

Then in the following weeks, we will talk about the natural gas markets, which I should be the focal point of any energy policy the US has that will bridge us from dirty energy like coal and oil to alternative energy like wind and solar. We will discuss LNG and what goes into making LNG, and finally give a detailed outlook on energy policy I feel would free us finally from the world chaos we call the energy markets.

As always questions or comments are welcomed.

I hope you enjoyed reading this as much as I did doing the research and putting this together. If you felt you learned something today, please forward on to others.

The only way to combat misinformation that is so rampant today is to spend time educating ourselves.

Have a wonderful weekend!!!