What Just Happened? 2022 The Year to Forget

What Just Happened? 2022 The Year to Forget

A Recap of how Central Bank and Government policies ultimately led to one of the biggest bubbles in history. A must read to understand how we got here and where we may be going

(I feel the below write up is something every person should understand. For too long, too few people have had total control of our wealth and economic outcomes. Unfortunately, it’s the worst off in our society that feels the effects the most when these policies reverse. It is not until everyone fully understands how the machine works that we can finally change it. With that in mind, if you find value in this information, please forward it on to others. It’s only through the sharing of knowledge that ultimate good change can happen.)

Cartoons of the Week (or year…)

The Quote of the Year for 2022:

“Oh, what a tangled web we weave when first we practice to deceive.”

Sir Walter Scott written in 1808

The End of 2022

Oh, 2022…..

You will go down as the year of inflation, but in reality, you were the year reality set in.

You were the year all actions from the great financial crisis and COVID responses caught up to us.

The year when many were again blindsided by the actions of their government and government agencies.

But mainly, 2022 will go down as the year of transition. A transition away from emergency policies that lasted too long and policies where we as a society got addicted to the outcomes.

Let us hope we can learn our lesson this time. The lesson that nothing is free and that everything has a cost.

To learn this lesson, we first have to understand the road that got us here.

So let’s take the next ten minutes to walk down the path of history over the past 12 years that led to the great inflation of 2022.

Less discuss…..

To Understand 2022, we need to go back to 2008

2008 was the beginning of the biggest financial collapse since the great depression.

We were literally a few days away from going over the cliff. Going where the world economy and monetary policy have never been before.

And while 2008-2009 turned out to be a very difficult time for most, it could have been much worse.

We were lucky to have a man in charge who has spent his life studying financial disasters and was the go-to expert on monetary policy during the Great Depression.

This man’s name was Ben Bernanke.

Hi, I am Ben!!!

In the middle of the Great Financial Crisis of 2008 (known as GFC), Ben introduced us to a few new terms.

The first was ZIRP (Zero Interest Rate Policy).

ZIRP was the policy of world central banks moving in tandem to push interest rates to 0%.

By pushing rates to 0%, it became cheaper to borrow money.

To make sure investors did not sell off bonds and in turn, try and push rates higher, he introduced us to a second term. QE (Quantitative Easing).

QE is a policy that pushes the envelope on free and fair markets.

What QE does is give central banks an unlimited amount of money to go buy stuff in the market.

When QE was introduced, it was used to buy any and all U.S. treasury bills or notes.

QE created an endless buyer of treasuries (government debt) in the market.

Once created, it pushed and kept our rates close to 0%.

As we entered 2009, another issue came up. The real estate market was tanking and mortgage rates were still relatively high versus where the Fed had put treasury rates.

As a result, with QE dollars, the Fed started to buy mortgages!!!

Creating a new endless buyer of mortgages in the market, rates on mortgages permitted, creating new demand for real estate in the United States.

Other countries like Japan pushed this policy even further. They started to use QE to buy stocks!!!

Both ZIRP and QE, along with those government bailouts, helped us get past the Great Financial Crisis.

But in the aftermath of this crisis, we faced new challenges the world has never seen.

The New World Order Central Banks Created

With interest rates near 0%, we started to see some extremely weird trends.

As you can see below, with an endless buyer of bonds, rates could go below zero!!!

As of the middle of 2021, nearly half of the world’s new debt had a negative interest rate.

In countries like Switzerland and Germany, if you took out a mortgage, the banks would pay you for that mortgage.

I promise you, this is something that has never been printed in any finance or economic textbook.

We were indeed in uncharted territory.

Investing Became Much Riskier

Another impact of these new policies was on investing.

Savers got punished while borrowers flourished.

With central banks now buying up all the bonds in the world, they took away the largest investment vehicles used by savers.

Investors were no longer able to see a rate of return on their checking or savings accounts. Normal bank CDs offered nothing. And if you tried to buy a treasury or a bond, the rate on those bonds was close to 0% (as you can see above).

What these new policies did was force you and everyone else who had a dollar to invest out on the risk curve.

As you can see below, the low-risk items in most portfolios went away.

In exchange for these low-risk savings, CDs, and bonds, people now had cash. And they were looking to put this new liquidity to work somewhere to earn a decent return.

As a result, we had more money chasing fewer and fewer investment choices.

This forced investors to take more risk while at the same time expecting a lower return.

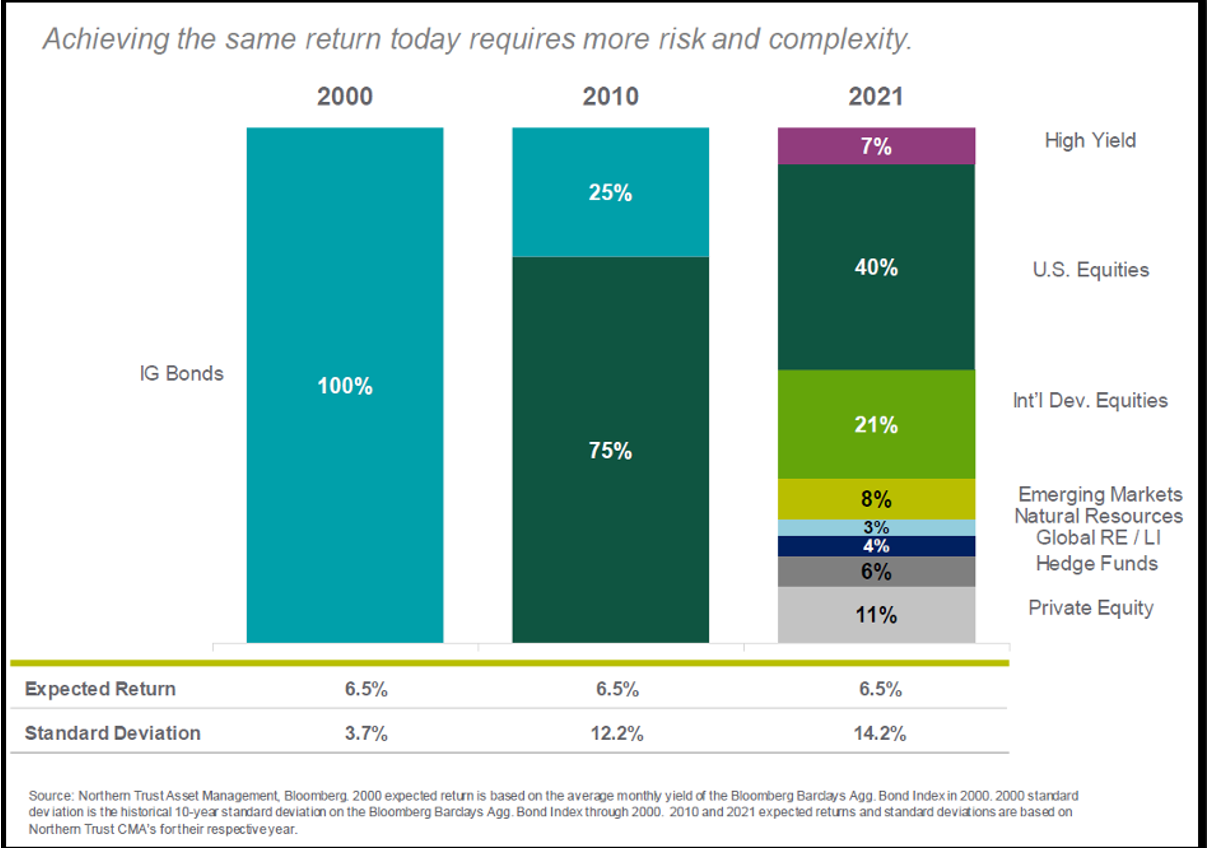

Below is a snapshot over time of the type of investments you needed to get a 6.5% return in the market.

In 2000, all you needed to do was invest in 100% bonds to get a 6.5% return.

Even in 2010, after the financial crisis and the start of ZIRP and QE, you were still able to get a 6.5% return, but you had to take on a higher risk.

But as more and more money chased fewer and fewer investments, the outlook of being able to get a 6.5% return became more complex.

By 2021, it was nearly impossible to forecast a 6.5% return without owning extremely risky assets like Natural Resources and illiquid and expensive assets like hedge funds and PE.

Investors Became Addicted to these Emergency Policies

Both ZIRP and QE helped us get through the Great Financial Crisis.

Both were extreme measures. Both were what we would call emergency policy.

But once the cat is out of the bag, it’s hard to put it back in. Investors quickly became addicted to this newfound liquidity.

Central bank QE measures became the only game in town. If you knew how QE was going to go, you could predict how the markets would do.

From stocks to bonds to real estate to crypto. It all moved as one and was all tied to the central bank’s liquidity (QE) policy.

Valuations did not matter. Economic outlook did not matter. All that mattered was how much more liquidity central banks would provide to the market.

Every time central banks tried to pull back from these “emergency” measures, the market moved lower.

As a result, central banks from 2009 through 2018 always reversed course and continued with these “emergency” policies even when the economy was doing well.

Enter the COVID Era

The start of COVID was a crazy time.

It was a time the world collaborated together to fight an unknown virus that threatened humanity.

Usually during periods like this, fear drives decision-making. COVID was no different.

As the economy of the world came to a standstill overnight, governments were scared of how this will affect their citizens both financially and emotionally.

Since we just went through one of the worst economic downturns in history 12 years earlier, many used this period as a roadmap for how to handle the COVID shutdown.

The first to act was the central banks.

Since QE worked so well during the Global Financial Crisis, they kicked this policy back into overdrive.

As you can see below, between 2008-2009, we added about $2-3 trillion in assets to central banks’ balance sheets (IE: central banks buy bonds and give investors cash and banks more reserves to lend to invest elsewhere).

In 2020, central banks amplified this significantly, moving from around $20 trillion in assets to $32 trillion in assets within 12 months.

At the end of 2021, central banks had over $32 TRILLION dollars of assets on their balance sheets.

This is enough to buy every public company in the S&P 500 (think Apple, GM, Microsoft, Google, Amazon, Nividia, Berkshire Hathaway, Ford, Boing, and 491 other companies) and still have $2 trillion left over!!!

With so much liquidity pouring into the markets, those who had money to invest quickly saw their investment returns skyrocket higher.

Take a look a the chart below. You can see, during the GFC, it took about 5 years for the top 1% to get to new highs in their wealth.

Looking at the same information for the COVID shutdown, they felt no real pain and quickly moved back to records. More importantly, the wealth created for the top 1% went vertical.

These policies did not only help the top 1%. Anyone who owned stocks, bonds, crypto, real estate, or any other investment saw their wealth explode higher.

If we zoom out of the chart above, the top 50% or so of citizens saw their wealth grow during COVID.

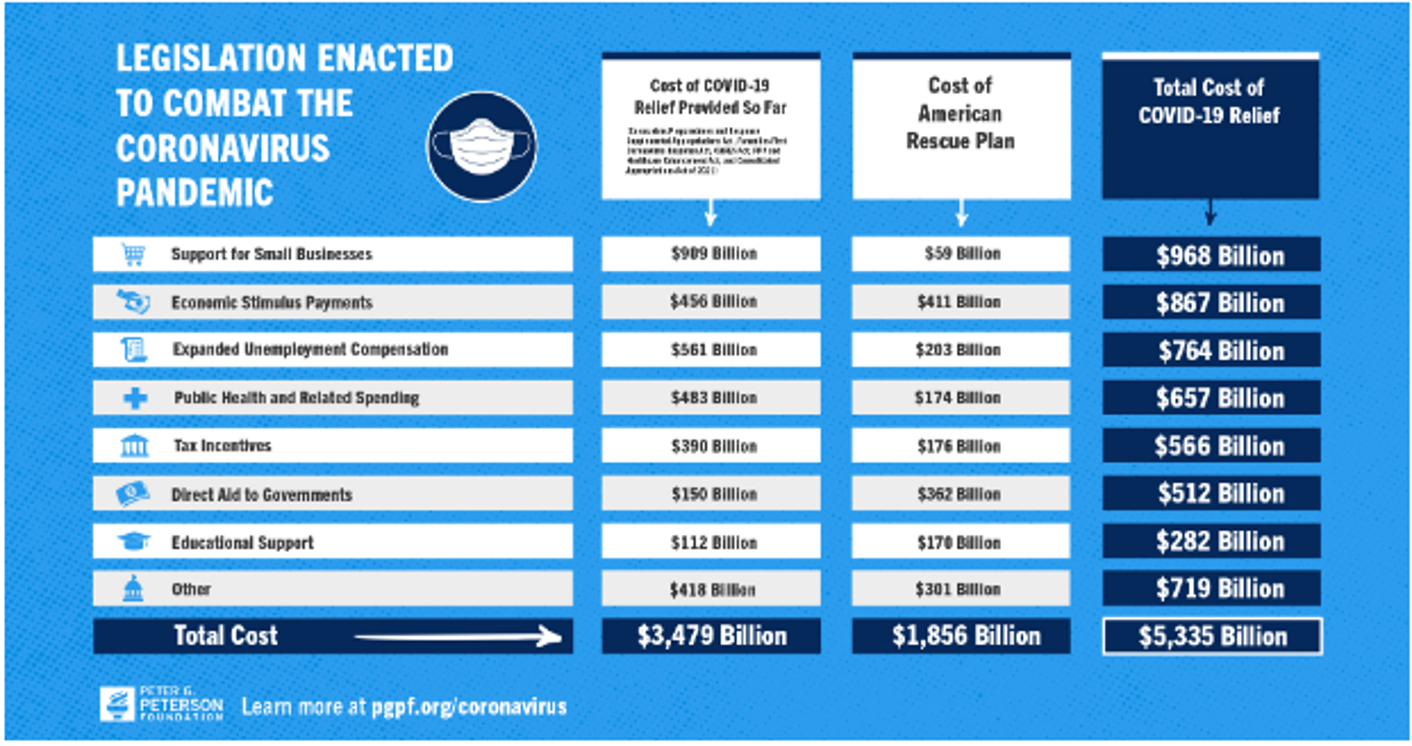

Enter Government Stimulus

Governments not wanting to be outdone by central banks also joined the party.

Legislation to fight COVID passed by the US government added another $5.33 TRILLION to the pockets of its citizens. And this was just in the U.S. Other governments around the world also implemented stimulus measures.

Much of the U.S. policy was in support of small business loans and stimulus payments.

This bill was a total bazooka policy. Let’s print endless amounts of money in a very short period of time and then pick up the cards later.

Looking at the chart below, pay attention to the orange line. This is government social benefits. The COVID policy that passed handed out WAY more money than was needed.

Everyone got rich off the government coffers. Government social benefits surpassed any other negative impacts we felt from COVID by a WIDE margin.

We were Drowning in New liquidity and Money

By the end of 2021, EVERYONE was feeling good about their financial situation.

With all the money given out by banks and governments, people were feeling wealthy.

As stated in Seeking Alpha:

“Over a 2-year period, from 2019 to 2021, household wealth increased by some $33 trillion, or over 150% of GDP.”

-Seeking Alpha Article

“Ignore the Wealth Effect at Your Peril” – June 30, 2022

We have never seen this type of increase in wealth in such a short amount of time.

All this newfound wealth needed to go somewhere.

It quickly got funneled into the stock market, which saw a new all-time high price 70 times in 2021.

It got funneled into real estate, which saw huge rises and record-level double-digit price increases in 2021.

It went into meme stocks which shot up 300%, 400%, and 700%!!!

It went into bitcoin and other crypto coins, which all made record returns and new highs in 2021.

And it went into new things like NFTs.

An NFT is “owning” a digital picture or art.

In 2021, the first NFT sold for $69.3 million dollars!!!!

That art picture is below. That is what they bought. Not something for the wall. They bought the thing you are looking at for $69 million. A digital original of that!!!

Not only did people invest their newfound wealth, they also spent it on stuff.

Tons of stuff.

2021 Supply Chain Issues

Have you ever wondered how that piece of fruit you just ate was able to get from South America to your store shelf before it spoiled?

How many people handled that piece of fruit? How many vehicles, trains, planes, and feet have been used to transport it? All that effort for less than a dollar.

That is the miracle we call the supply chain.

The supply chain has been expanding worldwide since the 1980s.

Over this time, the supply chain has become extremely efficient. As you can see below, prior to the downturn from COVID, the import and export supply chain were relatively steady.

This all changed in 2020. Both exports and imports plummeted lower as the world economy came to a halt.

All of a sudden, all those vehicles, trains, and feet used to bring you that piece of fruit stopped being needed. Many were laid off or fired. Many were forced to quit their businesses. Many in China were not even allowed to leave their houses.

What took decades to build was destroyed in months.

At the same time the supply chain was crumbling, we were implementing our money printing policies making everyone in the US feel wealthy.

With this newfound wealth, people demanded stuff.

As you can see above, our demand for imports spiked higher and quickly surpassed our normal trend of demand. This happened at the same time our supply chain was crumbling.

As a result, there were shortages of goods everywhere.

And when you have too much demand for goods and not enough supply, something has to adjust. And usually, that something is prices moving higher.

Welcome in Inflation

The combination of central bank policy stimulating the top 50%, with the free money handouts stimulating the bottom 50%, combined with new supply chain issues, we had the perfect recipe for disaster.

There was too much money chasing fewer and fewer investments and goods. Something had to give. And what give was the price of these items moving higher.

While we have seen inflation in the investment markets for years (what some would call good inflation), this now carried over to the price of goods (what some would call bad inflation).

We saw inflation go vertical as we entered 2022.

Something had to be done…

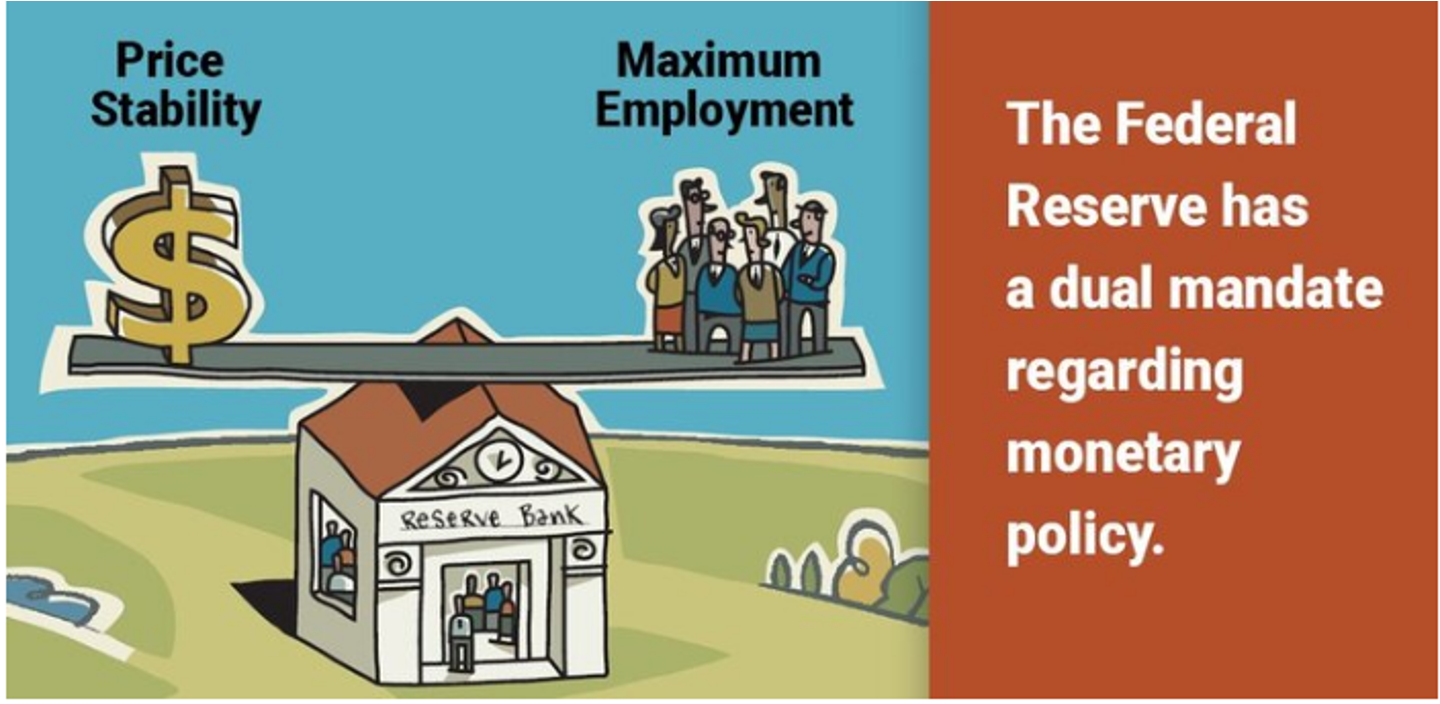

The Fed’s Dual Mandate

The Federal Reserve has what is called a dual mandate.

Their goals are to keep the economy at max employment while keeping prices stable.

As we entered 2022, U.S. inflation was at a new 40-year high (internationally was worse).

At the same time, U.S. unemployment was at a 50-year low.

If you have a dual mandate stipulated by congress with one of those mandates at a 50-year low and the other at a 40-year high, which one do you think you would focus on?

You got it….Get inflation down at all costs….

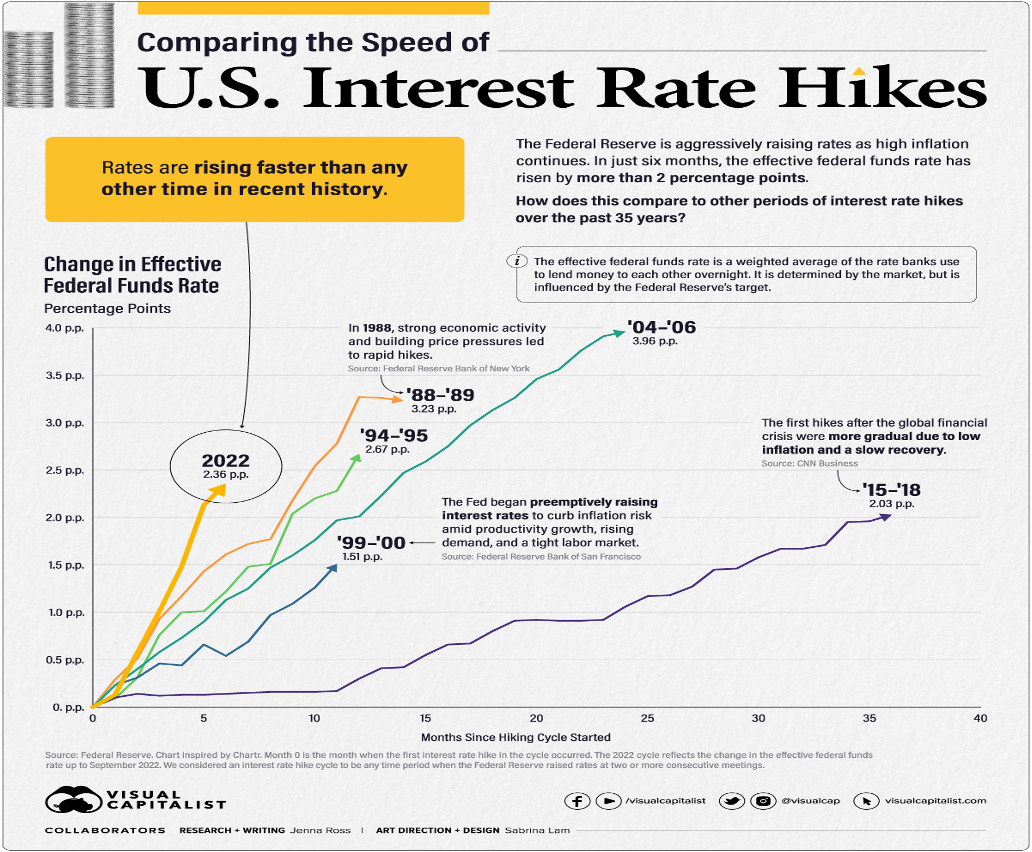

To do that, the Fed’s goal was simple. Make you feel poorer by pushing the prices of investments lower. And to do that, they reversed the policies they implemented over the previous 12 years.

As you can see below, 2022 will go into the record books as the fastest interest rate hike in history (and we are still in the middle of this moving into 2023).

When you have such a reversal of policy so quickly, EVERYTHING has to adjust.

The first place adjustments where in investments and real estate.

Bond prices have adjusted quickly and continue to adjust to the new policy as I type this.

People can again invest money in bonds, CDs, and savings accounts.

As a result, you see investors selling both long-term bonds and stocks and investing in cash.

If we ended the year in September, 2022 combined stock and bond returns would have gone down as the worst year for performance in the last 100!!!!

Data as of the end of September 2022. Markets have moved higher since.

When it comes to Real Estate, we are seeing the same impact.

Buyers are no longer able to afford higher prices because mortgage rates have moved from 3% in 2021 to nearly 7% in 2022.

Sellers, who just saw their neighbor sell their house for a record amount 6 months ago, are not willing to lower their prices.

As a result, the real estate market right now is at a standstill. Last month saw a record drop in sales. We have never seen a faster drop in the history of this data!!!

And as for the Crypto market. Don’t even get me started :)

In essence, what we have experienced in 2022, and continue to experience as we enter 2023, is the market reversing 20 years of policy in less than 2 years.

As you can see below, rates around the world are again positive.

We will all be better off after the adjustment is over.

The markets will get back to some type of “normal” trend we have experienced since World War 2.

Central Bank actions will no longer control every market and create massive bubbles everywhere.

All of these things are good things.

The key question is how long will this adjustment take, and how will it end.

How it Ends

The short answer is - only time will tell. I will try my best to address this question next week, with the caveat that short-term crystal balls are very foggy.

In the meantime, we do know a few things.

First, the market moves on investor emotions. As you can see below, I think we may be in the denial/fear stage of this cycle.

We have yet to see real panic or despondency or depression.

You probably have heard the term “soft landing”. This term means central banks trying everything in their power to cut the downturn off at fear and not go any lower.

Only time will tell if they will be able to accomplish this task.

We also know investing is both an art and a science.

The art part of investing is the short-term swings. No one knows what will happen in 2023 or 2024.

All we know is that the market will do what creates the most emotional pain in the short-term for the most amount of people.

The science part comes when we talk about investments over the longer term.

Over the long term, markets go up. If you believe in capitalism and the US economy, then you believe that over the long term, investments will go higher.

Looking at the chart below, while rolling 1-year returns can have big moves in both directions, when we get out to 10+ years, we can almost pinpoint what your returns will look like over that time.

This is the science of investing.

Focus on the science and not the art and you will be better off.

Final Thoughts

We are again in the middle of another man-made economic downturn.

Our audacity to think we could print endless amounts of money, charge no interest on this money, have prices of everything rise, and make everyone feel so “paper” rich without any ramifications was just more hubris from our world leaders.

Now the Fed is again trying to generate a “soft landing” and make up for its bad policies over the last 12 years.

So far, so good.

Mainstreet continues to do well while Wall Street is taking a beating.

Let’s just hope the pain Wall Street felt in 2022 does not come knocking on the door of Main Street in 2023.

Next week I will break out my crystal ball and try to give you an outline of how 2023 may play out. As I stated above, proceed with caution with any short-term predictions. That being said, it’s still worth the time and energy to go through the analysis and process.

Have a Great Weekend!!!