The Twelve Most Powerful People in the World You have Never Heard of....

The Twelve Most Powerful People in the World You have Never Heard of....

The Federal Reserves voting members are trying to make a slow exit, but they seem like they can never leave.

Quotes of the week:

“Last thing I remember, I was running for the door, I had to find the passage back, To the place I was before, "Relax, " said the night man "We are programmed to receive, You can check out any time you like but you can never leave."

-Lyrics Hotel California by the Eagles

“Nearly all men can stand adversity, but if you want to test a man’s character, give him power”

-Abraham Lincoln

Cartoons of the Week:

Quick Question for You

I have a quick quiz for all of you today.

Look at the picture below.

Do you know who these nineteen people are?

Can you name more than one or two of these people?

I would say 99% of the American public could not name more than one or two of the people in the picture above.

But 12 of these nineteen members have decision-making rights that are up there in importance with the President, Congress, and other major world leaders.

Some would argue this picture shows the most powerful group of people in the world, at least when it comes to your financial well-being during peacetime.

The list of these nineteen people’s names is below. Only 12 of them vote on policy any given year.

These twelve voting members can make you feel really rich, or make a few adjustments in their decisions until you potentially get fired from your job.

They can make money basically free or can push interest rates high enough that you will never be able to pay off that credit card debt.

To give you an example of the power they have, from March 2020 to March 2022, they decided to create $5 TRILLION dollars and place it into our economy.

We did not vote on it. We had no debates. It just happened.

Actions like this by these twelve voting members would have been unprecedented from 1940 to 2007 but now are commonplace since 2008.

I talk so much about the Fed because they are such an incremental part of our economy and personal financial well-being. I don’t like talking about them but the fact remains, they single handily control everything.

This group of strangers decided again this week to increase interest rates by another 0.25%, to the same level we saw rates prior to the 2008 financial crisis.

This is happening at the same time we face the biggest banking crisis since 2008 when viewed by asset size.

To be clear, this current banking issue is NOT 2008.

In fact, it is the exact opposite of 2008.

In 2008, we had a credit issue. In 2023, we have a duration issue.

It is a crisis formed, created, and executed by these nineteen members. This crisis is 100% the result of the Federal Reserve.

The potential upcoming recession and hard landing we will probably go through is also 100% the result of the Federal Reserve.

By pouring $5,000,000,000,000.00 into the economy in a 24-month period (that is only $208,300,000,000.00 a month), they swamped everyone with liquidity. Add the Federal Government stimulus, and it quickly overheated our economy.

This liquidity and money had to go somewhere. It created an exponential rise in Bitcoin, made NFTs and .JPG pictures of monkeys worth millions, it helped push stocks to crazy elevations, and made this thing we call a house below worth a HALF A MILLION DOLLARS!!!

Would you pay $500,000 for that? Yep, things have gotten a bit out of hand.

A big chunk of this “liquidity” also went into banks.

And when banks take in uninsured deposits, they need to buy something with those deposits to make a profit.

But when rates look like the below chart,

Some banks saw the only place to earn money above the 2% inflation rate was to purchase 20-year or 30-year treasury bonds. Others saw higher rates in mortgaged back securities and agency debt, so they bought that stuff.

If they bought treasuries, which are called “risk-free” assets, then they are not, by name, taking any risk with these investments.

But when those same twelve voting members of the Fed decided they made a mistake, and now faced an inflation spike that was going out of control,

They tried to whipsaw their policies as fast as possible, setting records for the fastest rate hikes ever.

While at the same time trying to shrink their balance sheet (first red arrow).

All this liquidity draining at record levels has now pushed M2 (the base measure of money supply in the system) to a growth rate below zero for the first time in history going back to 1959!!!

We have never seen our money shrink year-over-year till now, 2023.

And the banks, who were the main recipients of the Fed’s Givith policies, are now dealing with the Fed saying to them….

“When rates go up, things blow up.” – Wall Street Saying

So now some Regional Banks are in a bind.

As the token 12 members of the voting Fed quickly tried to reverse their policies, the hangover effects are just now taking shape.

When we look at economic activity overlaid by the Fed Funds Rate, we can quickly see where this thing may be headed.

But, let’s forget about these ugly forecasts for a moment and just focus on the banks.

Those same banks who looked to buy 20- and 30-year treasuries, or mortgage securities, are now seeing MASSIVE losses from those holdings.

But, because of a few accounting gimmicks, we do not really see these losses in banks’ earnings or accounting reports.

Why you may ask.

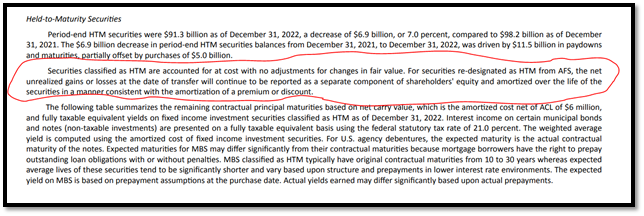

Because of an accounting term called “Held-to-Maturity”.

Banks are allowed to buy bonds or other securities and as long as they hold them until they mature, they do not have to show any mark-to-market losses. All mark-to-market loss is showing daily fluctuations in price in the market.

You and I do not have that luxury.

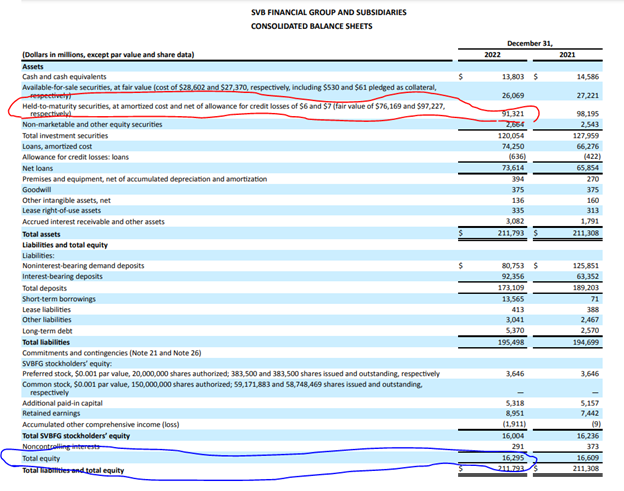

Just take a look below at Silicon Valley Bank’s 10-K report filed on February 24, 2023.

Look at the column that says HTM Securities (HTM = Held to Maturity).

As of the end of the year 2022, SVB held $91.3 billion in assets in “Held to Maturity”.

As you can see below, these are “accounted for at cost with NO ADJUSTMENTS FOR CHANGES IN FAIR VALUE”.

What does this mean?

It means even if these bonds have moved significantly lower in price, because of the rapid rise in interest rates from the twelve token members of the Fed, they do not have to show any of these losses.

As anyone who owned a bond last year quickly found out, when interest rates go up, bond prices fall.

Even if you or I had a bond in our account, and wanted to hold it till it matured, we still saw the losses on our statements from the price declines.

But not these banks.

Look at the average interest rates of the bonds “held to maturity” at SVB in the right-hand column below.

When you have low yields and see rates move up as fast as they did, there is going to be a drastic drop in the price of those bonds.

If we use the analysis below from SVB 10-K, which states the average duration of these securities was 6.2 years, we can quickly calculate what the losses may be.

If the average interest rate was 1.66%, as stated above, and the 5-year treasury was around 4.00% in March 2023, then we can back into the potential percentage loss:

(4.00% - 1.66%) * 6.2 = a percentage loss of about 14.5% on this portfolio, or $13.25 billion dollars.

So when we look at SVB's balance sheet, you can see they still show those “held-to-maturity” bonds at the value they bought them at (red circle), the market quickly understood these assets would sell in the market today at a much lower price then what is being shown below.

Using our back of envelop calculation, we came to a $13.5 billion dollar loss on those securities.

In mid-March, when SVB problems started to show up, the 5-year treasury moved up to 4.30%. The higher the interest rates move, the bigger the loss was for SVB.

At a point in March, the loss on the “held-to-maturity” securities alone where larger than the total equity of the company (blue circle above).

This is the definition of insolvent; bankrupting your equity holders.

As a result, bank depositors pulled their money and the Fed needed to come and rescue SVB before they were totally insolvent.

But none of this would have mattered except for the fact the famous investor Peter Thiel started to tell companies, private equity people, and friends who had money at SVB to pull their money out of the bank.

And once the “experts” start to do it and others got whiffs of this news, everyone starts to do it.

And in a blink of an eye, SVB (Silicon Valley Bank) was in need of money to cover all the withdrawal requests from their depositors.

With no money left to cover all the withdrawals, they were forced to show their hand and to show everyone their losses on the “held to maturity” securities on their balance sheet.

The twelve members of the FOMC who voted on throwing endless amounts of money into the system in 2021-2022 only to reverse it at record levels in 2022-2023, missed this one little issue.

The thousands of members employed by the FOMC, who regulate banks like SVB, missed this so simple of a problem.

“When rates go up, things blow up.” – Wall Street Saying

We all know you cannot turn a ship too quickly otherwise bad things happen. Just like the video below of a Carnival Cruise ship, our policymakers have turned the ship too quickly, creating destruction for everyone on board.

So now here we are, with the Fed on one hand taking liquidity and money away from the system at record levels.

On the other hand, they are trying to put out fires they have created by giving emergency facilities to banks and other institutions (ie: printing money again).

The Fed is trying to control everything.

But when you try to control everything, you end up controlling nothing.

And while they have tried so hard since 2018 to back away, as the quote at the beginning says, “You can check out any time you like but you can never leave.”

Because of their errors, we saw many bubbles form only to pop last year. We almost saw the entire pension system in the U.K. implode.

Today these twelve members of the Fed are continuing to raise their rates and pull their liquidity which is now whipping out billions of dollars in value at regional and local banks.

Destruction ALWAYS lies in the Fed’s path as they try and fix their mistakes. We are in the middle of one now, so beware.

Mistake #1: Cut Rates to Zero and Expand the Balance Sheet

Mistake #2: Inflation is “Transitory” and will go away soon

June 2021 Powell Statement:

“We tend to use [ transitory] to mean that it won't leave a permanent mark in the form of higher inflation,” Powell told Senate lawmakers.

Mistake #3 - Raising Rates too Fast Because of mistake #2…also cutting their balance sheet at the same time

Potential Mistake #4: Banking System is Fine

May 2023 Powell Statement to the Press:

“The U.S. banking system is sound and resilient.”

But the market would really really really disagree with this viewpoint. Just look at some of these stocks.

Banking Charts: (down and to the right is bad)

Have a wonderful Weekend!!!