RadioShack'd - The Tune of US Consumer Debt Today

RadioShack'd - The Tune of US Consumer Debt Today

We take a look at RadioShakes final Days and How it Relates to the Debt Levels of the US Consumer Today, Wrapping Up with some Tunes for your Weekend...

Cartoon of the Week (It’s about Me):

Quick Story

Back before there was Amazon, Wal-Mart, Best Buy, or even Circuit City, there was a company named RadioShack where everyone went to see and buy the coolest new electronics.

Growing up in Chicago, my friends and I would always look to save up a few bucks and walk down to Irving Park Road at Six Corners to visit RadioShack. It was an upstairs storefront, and below it was a Ninja Shop. Between those two stores, we never walked back with money in our pockets. After all, who can resist electronic cars, walkie-talkies, talking robots, and Chinese throwing stars? What a great combo.

From The Shack’s early days in the 1920s, as a specialty electronics store, it turned into the juggernaut of its era in the late 1970s and early 1980s, having stock price returns as large as 50%, 200%, and even 350% per year. RadioShack was growing across the country, peaking with over 8,000 stores fronts by 1999.

But like many of the stores from my childhood (IE: Toys-R-Us), RadioShack fell on hard times after the turn of the millennium.

By 2012, they were straddled with a ton of debt, and their equity (i.e. stock) price was plunging.

They were running out of cash quickly.

At that time I was the Portfolio Manager of a Capital Structures Opportunity Fund, a hedge fund specializing in taking advantage of mispricings in company capital structures.

In the 3rd quarter of 2012, we entered a position in RadioShack, going long their senior bonds, which were yielding over 13% at that time, and going short the stock, which was priced close to $10 a share at the beginning of the year but was quickly losing value. Our short price on the stock was a little over $5 per share.

We saw no way RadioShack was going to make it past its wall of debt coming due.

Best cash scenario: They try to refinance their debt for much higher yields. In this scenario, we would get paid 13% while we waited and see our bonds refinanced at par, only to put more burden on the stock holders with higher interest costs.

Base Case Scenario: They would be forced to file bankruptcy, pushing the stock price to near zero while as senior bond holders, we would be the first in line at the bankruptcy table to cash in on their assets.

This is what you call an asymmetric opportunity and what everyone in the financial markets looks for to create “alpha”.

As debt holders and analysts of their balance sheets, we saw the writing on the wall for RadioShack before equity holders saw it. Cash was running out quickly, they had a convertible bond coming due in mid-2013, and the stock was extremely expensive relative to the bonds.

At the end of 2012, RadioShack’s stock price was at $2.12 per share, while its senior bonds were down minimally.

In 2013, the stock did better as they secured some additional financing, but being long the bonds, we still received a great return from bond price appreciation and interest payments, more than offsetting any excitement from the stock we were short.

By the middle of 2014, RadioShack’s cash levels were only $30.5 million dollars, down from $432 million dollars only a year prior. At the same time, their debt profile ballooned to over $656 million.

More importantly, they were burning through $50 to $100 million each quarter.

With all this negativity, It was not till 2014 that the debt burden finally caught up to them and the stock went into free fall, going down to only $0.37 cents by the end of 2014 and $0 by February 2015 when they filed for bankruptcy.

Looking back at this trade now, I have a few takeaways:

While the writing was on the wall in early 2012, it took another 3-years before the bankruptcy filing happened.

Debt burdens are hard to maneuver around. It’s like a weight tied to your foot while you are trying to swim. You may stay afloat for a bit, but eventually, the weight will take you under.

Right when things get tough, banks and investors look to compensate themselves for higher risk by increasing interest costs or shutting down access to capital altogether.

When I look at this trade in RadioShake, I cannot help but see the parallels now with the U.S. consumer, debt levels, and what is happening with equity prices.

The U.S. Consumer Today

I talked last week about the U.S. debt downgraded by Fitch, which stated because of our country’s huge and growing debt burden, we are no longer a AAA debt-rated country. You can read that HERE.

Wearing my analyst hat today, I would also be downgrading the U.S. consumer as well.

Debt levels for the average consumer are climbing at alarming levels, right at the same time interest cost are exploding higher.

Per Creditcard.com, the current average credit card interest rate is 20.93% !!!

This number is expected to climb in the coming months to surpass 21% for the first time ever!!!

Out of the 100 cards they track, 14 of them have interest rates over 30%!!! These are usually the ones issued to the consumer with the worst credit score.

This is happening at the same time credit card balances are exploding higher, surpassing $1 trillion for the first time ever.

The largest of this debt falls on middle-aged generation X’ers, like me, ages 40-49, who have an average credit card balance of $7,600.

But across all age groups, credit card balances are rising.

This is on top of the $1.78 Trillion in student loan debt that will need to start being repaid next month.

And while 90% of this debt is federal, with locked interest rates between 4.99% to 7.54%, 10% of this debt is variable in nature, with rates ballooning higher over the past year during the student loan no-pay holiday.

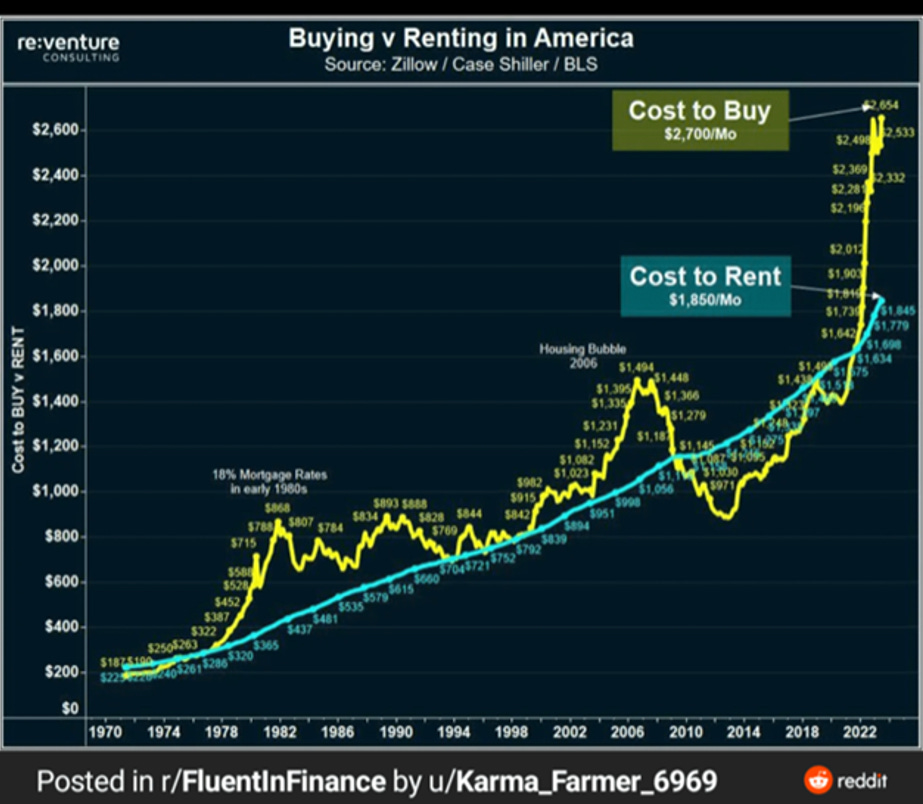

On top of this, we have home affordability issues, which is the lowest we have seen since the 2007 bubble.

This is pushed by prices continuing to stay strong while interest rates continue to march higher.

When you look at usdebtclock.org, you can see just how crazy prices have moved in relation to household median income over the past 23 years.

When compared to renting, buying now looks like a stupid decision.

But even with the recent rental price increase, the average renter is now paying 30% of their median income for rent.

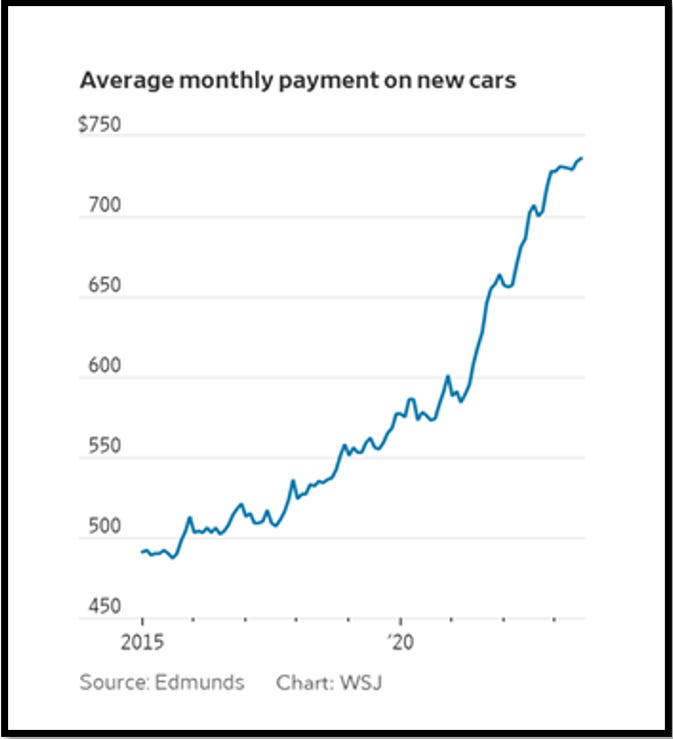

In addition to credit cards and rent, car loans are exploding higher as well.

A Tahoe, which I recently purchased, sold for $35,000 15 years ago, now is $85,000.

At the same time, interest rates on loans have moved up into double digits on used cars and nearly 7% on most new cars.

This has pushed the average monthly payment on new cars to nosebleed levels.

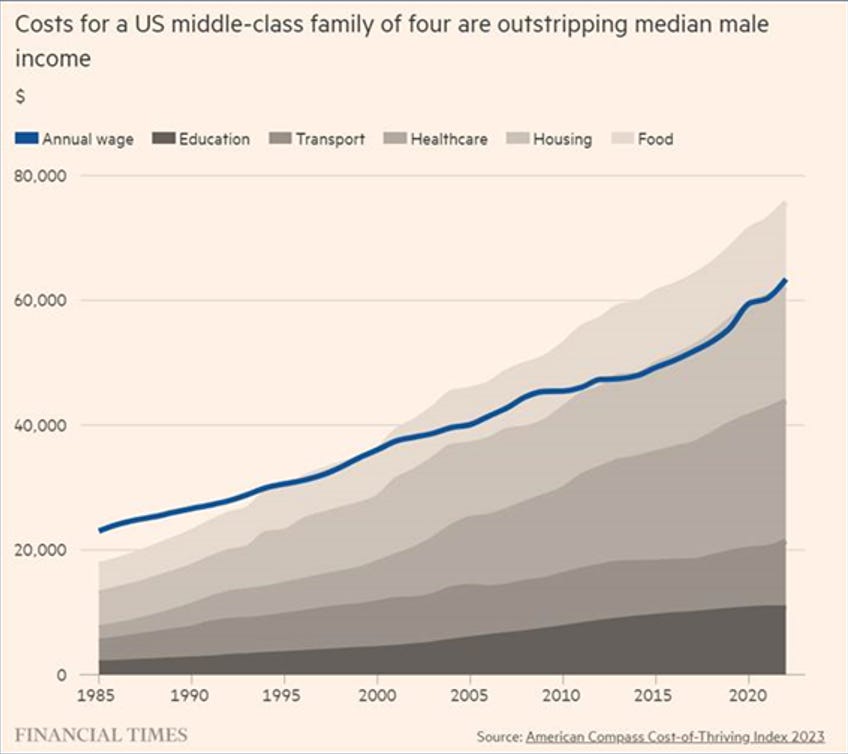

All in, per the New York Fed’s quarterly Household Debt and Credit Survey, total consumer debt now stands at $17 trillion as of the first quarter of 2023. This is a new record high.

Combine this increase in debt and interest payments with the cost of living issues we have faced over the last year, and it’s becoming very difficult for a family of four to make ends meet.

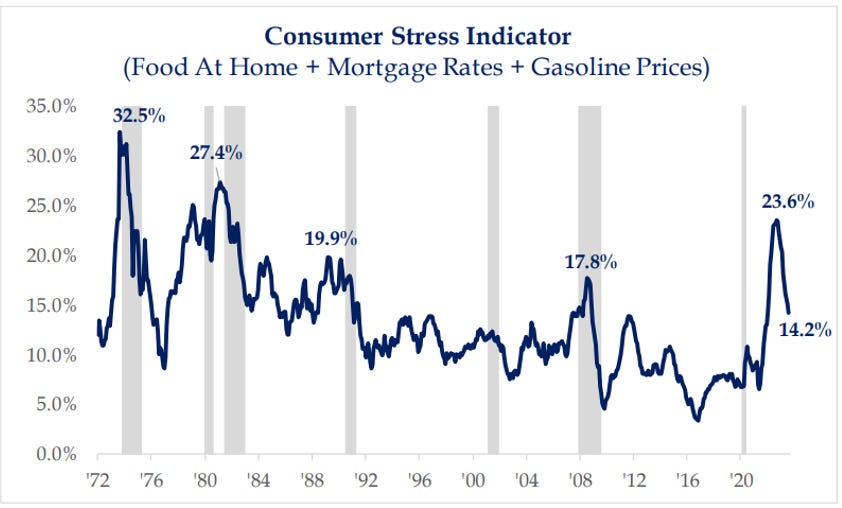

The one positive is that the stress of all this has been subsiding so far this year, which is having many feel the worst may be behind us.

I am worried about the hangover effect, which has not hit the market fully. Just look at the above, the gray areas are recessions. Usually, the peak in stress happens before the recession kicks in.

Only time will tell if this time is different.

Final Thoughts

While the writing seems to be on the wall when we look at data, just like RadioShack, how long will it be before everyone gets exhausted treading water and starts getting pulled under by the weight of it all?

Sitting here today, with my analyst hat on, just like I did with RadioShack, it is hard to see how this ends well.

It may be different this time, or I may be missing something, but it’s hard to see you as a consumer continuing this trend.

That being said, a company like RadioShack, which was destined to fail, still took 3-plus years to finally collapse.

Will the U.S. consumer be as resilient?

I find it hard to imagine we do not see some sort of adjustment.

Right now interest rates have been adjusted by 500 basis points but, it seems, nothing else has been adjusted. This is not sustainable, in my view.

I wanted to end with this……

Throughout history, music has always spoken the word of the people during that time period.

In the 1960’s and 70’s it was songs like “For What It’s Worth” by Buffalo Springfield,

or “War” by Adwin Starr,

or “Fortunate Son” by Clearwater Revival.

This all changed by the 1980’s when we as a society felt good about things again.

That environment produced Madonna, Cyndi Lauper, and Michael Jackson,

with hit songs like “Hit Me with Your Best Shot”,

or “Here I Go Again” by Whitesnake

or one of my favorites, “Break my stride”,

All super uplifting and in line with the way people felt in the 1980s - happy, excited, and go and get after it attitude.

It was all wrapped in a general feeling of pure optimism of real change for the better, as outlined in the song “We Are the World”.

Even in the 90s with grunge and hip hop, and what I would argue is the best genre for music, we still had songs like “Steal My Sunshine” by Len which I think represents the 90s perfectly.

Then 9/11 happened, and it changed everything.

Songs went from happy to sad and mad.

We had songs like Alan Jacksons’ “When the world stops turning”, which still brings tears to my eyes.

And the anger with songs like “Courtesy of the Red, White, and Blue” by Toby Keith.

So if you agree music speaks the voice of the era, what does it say that a song by an unknown artist named Oliver Anthony, who recently put out a song online called “Rich Men North of Richmond” is going viral?

It starts:

“I have been selling my soul, working all day, overtime hours, for BS pay, sitting out here, and wasting my life away.”

Music is the voice of the times. Right now, the average American is struggling and close to going under.

I hope and wish I am wrong. But just like RadioShack in 2013, just because things look a little better on the surface does not mean they are improving under the surface.

Have a wonderful weekend….