Let's Talk About Bonds Baby, Let's Talk About You and Me...Let's Talk About all the Good Things and the Bad Things That Can Be (in fixed income)

Economic Perspective of the Week - Week 16, 2022 Fixed Income and Bonds 101 - Primary and Secondary Markets along with Credit Risk

Cartoon(s) of the Week:

Quote(s) of the Week:

“When growth is slower than expected, stocks go down. When inflation is higher than expected, bonds go down. When inflation is lower than expected, bonds go up.”

- Ray Dalio

“I’m just trying to get used to living on a fixed income. Now it is going to get unfixed.”

– Janet Jackson

Most of you have now received your first quarter 2022 performance reports, statements, or investment snapshots for the quarter and saw the return and were like this mem below…..

We just experienced the worst quarter since the pandemic downturn in March 2020. A downturn is to be expected after the last 3 years of fantastic returns. But when you look across the board, the only thing that was up was commodities.

Everything else was down……

Negative returns are part of the game. But this quarter, one thing stuck out. It was the first time in a long time both stocks AND bonds were down in the same quarter. Since 1976, this has happened only about 10% of the time. It’s rare…

More importantly, those who invested in “safe” bonds saw their returns there down more than equities or “risky” high yield bonds.

What is that about????

Because of all the questions I have received on this topic in the past 3-5 months, I wanted to put together a fixed income investing 101.

This will be made up of two parts.

In part 1 we will focus on what is a fixed income investment and what exactly is credit risk. Part two we will focus on a big hidden risk in the market today called duration and outline for everyone how you should think about investing in fixed income moving forward.

What is fixed income?

Let’s start from the very basic.

The world operates today because of capital (another word for money) that people “invest” to make money on their money.

As Ray Dalio so elegantly stated:

“Every investment is a lump-sum cash payment now for an income stream in the future.”

When Tesla wanted to build their Gigafactory, the initial cost is over $1 billion with estimates back in 2014 of a total cost of $4 - $5 billion.

To build this giant factor, Tesla had to make a decision.

Since they did not have the cash at that time, where will they source the capital to build the factory?

They could either issue equity in Tesla stock (issue more stock) which would dilute Elon’s ownership OR issue bonds.

Tesla decided in 2013 to issue bonds (specifically convertible bonds which we will discuss later) and continued this trend for the next 6 years.

In 2013 they issued $600 million in bonds

In 2014 issued $2 Billion in bonds

In 2017 issued $850 million in bonds

In 2019 issued $1.6 billion in bonds

As an investor, when you invest in a stock you are taking ownership of that company. As an owner, you are the last to get paid but also have the greatest upside if things go well.

With stocks, you are looking for a return ON your money.

With bonds, you are lending a company or government money with the idea they will pay a certain yield or return over time and in the end, you will get your money back.

With bonds, you are looking for a return OF your money.

Inputs you need to know about a bond:

There are four different numbers we need to focus on to understand how bonds work.

The first is the bond's face value. Most bonds have a face value of $1,000 per bond.

The second input is the coupon or yield of the bond. What are you getting paid to own that bond?

The third is the price of the bond. Most bonds at issuance are priced at $100 which is known as a bond’s “par” price.

Bonds are priced in an even $1,000 value to make it easy for the investor to determine how much money they will make off the bond.

If you buy one corporate bond with a coupon of 6%, you will get paid $60 a year to own that bond until maturity ($1,000 times 6%).

The length of the bond is how long until the bond matures. Once a bond matures, you get your $1,000 back.

What are the Risks of Investing in Fixed Income or Bonds?

Bonds have two unique risks.

1. Credit Risk

2. Duration Risk (we will talk about this next week)

Credit Risk

Credit risk is the easier of the two fixed income risks and the one we will talk about this week.

Credit risk is the risk that when you lend money, you will get paid back.

Since we do not have a crew of guys like this…..

Investors use laws, courts, and bankruptcy processes to get their money back.

In the case of Tesla, if they ended up not making it and filed for bankruptcy, the bondholders would in theory “own” the Gigafactory and other assets of Tesla while Elon Musk would have nothing.

This is because, in bankruptcy, bondholders get paid before stock and equity holders. This is called a “capital structure”.

In bankruptcy, a court will determine the value of a company’s assets, sell those assets off, and then distribute the proceeds in the order outlined by the company’s capital structure (picture above it would be the senior secured bondholders get paid first).

Once those holders get paid back in full, what is remaining goes to the senior unsecured bondholders. This process continues until there is no money left.

This is called a “waterfall payout”.

Think of it as water getting poured into buckets starting at the top and it will not overflow into the next bucket below until totally filled.

When you hear of a company “reorganizing”, instead of selling its assets, it will file for bankruptcy and value the company at its current value in the market.

From there they will issue new stock and give it to the bondholders. Again, this process is like the waterfall outlined above, which usually ends with the common stockholders and preferred stockholders receiving zero on their initial investment. They basically get whipped out.

This is what the airline companies did in the financial crisis. Many filed bankruptcies but are still operating today. They just whipped out their stockholders, made their capital structure smaller, and continued business as usual.

This is why stocks are more “risky” than bonds. If you know what hits the fan, you are the last one in a very long line of people to get paid. The majority of the time in bankrupcies, the equity holders get nothing.

BUT, as with what happened with Tesla, if the company does well, the bondholders only get paid the coupon or yield on the bond and nothing else. All corporate “value” flows through to the equity holder (flows to the bottom of the capital structure picture above).

Starting at the top of the capital structure, everyone gets a fixed payment on their investments. After you have paid everyone, any value remaining goes all to the equity holder.

In the case of Tesla, its stock price rose from $5.74 in 2011 to $1,229 at the end of last year. If you invested $1,000 in 2011, it would be worth $204,000 at the end of 2021.

The bondholders (in theory) saw none of this gain which flowed through to the equity holders and is what made Elon Musk the richest guy in the world last year. He owned none of Tesla bonds but did own a majority of Tesla stock.

How is credit risk determined?

When a company comes to the market to issue a bond, it does a roadshow to visit investors.

As an analyst for an $8 billion dollar high yield mutual fund, I sat through a few hundred roadshows in my day.

The company’s management team goes on the road to meet investors in person, usually in the big cities around the world over a 3-5 day period. They would give a presentation like the one below from Monsanto, outlining how great they are and why you should loan them money.

Once finished, the investor or analyst goes back to their desks, runs a bunch of numbers and projections, compares these numbers to other investments, and lets the banks know what type of yield they want in exchange for a portion of the bond.

Depending on the quality of the company, the probability of it going into bankruptcy, where the holder would be paid in a bankruptcy, and the price and value of similar bonds in the market, the yield on the newly issued bond is determined.

With the four inputs we discussed earlier, the goal here is to determine the coupon of the bond and the length of the bond.

The bond’s face value and the price stay constant.

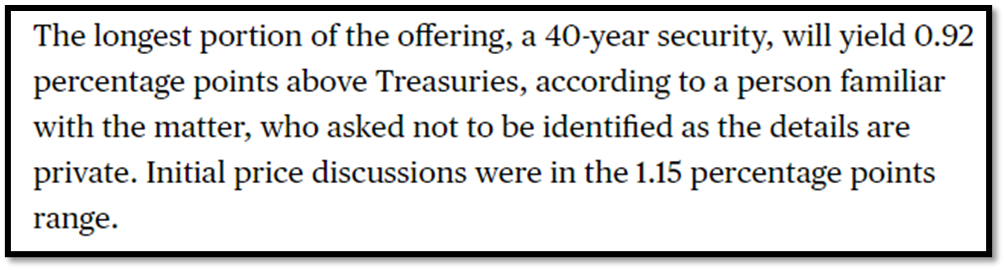

In the case of a company like Apple, in the middle of 2021, they issued $6.5 billion dollars in bonds.

One of those issues matures in 2061 and pays a yield of 2.80%.

Another bond for $1 billion matures in 2031 and pays a yield of only 1.70%!!!

Notice it’s in the same bond “issuance” BUT within that offering, we have different bond coupons and lengths of bonds.

The larger the size of the offering, the more tranches it may have with different coupons and maturity dates.

Now let’s compare Apple's issuance last year to Ford Motor Company, which is issuing debt now for $1 billion.

Right now the analyst are running their numbers and have determined this should have a yield of 5.25% (you can see below at the end).

Or VistaJet, a small private client airline, is looking to issue $440 million in debt. You can see analysts are “whispering” the mid 8% range with banks pushing for a price closer to 8.25%.

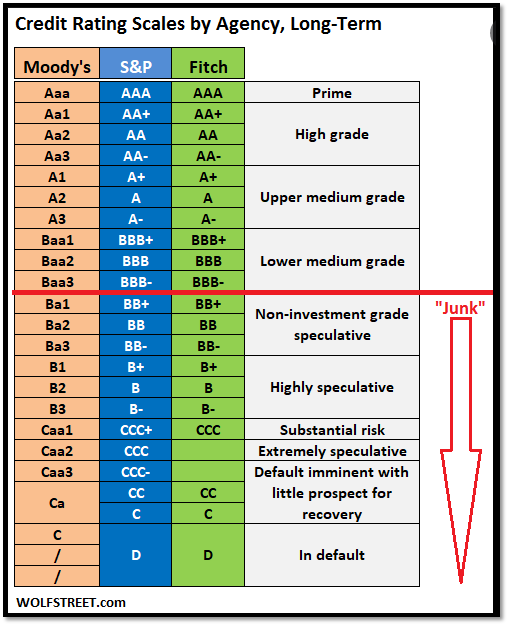

Those companies that are high quality like Apple usually get rated by credit agencies as Investment Grade Bonds.

Investment grade bonds have a low credit risk (what are the odds Apple goes bankrupt in 10 years…very, very small) but HUGE duration risk (we will discuss next week).

Companies like Ford Motor and VistaJet are higher-risk companies of bankruptcy and as a result, get rated by credit agencies as High Yield Bonds or Junk Bonds for short.

Above, default is another word for bankrupcy

High Yield bonds historically are much higher credit risk (odds between 10% and 50% you will not get your money back) but historically very low duration risk (we will talk about next week).

What you need to know for now is this.

When the economy is doing well, you want to take credit risk and not duration risk.

When the economy does poorly, you want no credit risk and want to take of duration risk.

All bond yields are priced at a rate above US government debt.

From the article above about Apple issuing bonds, notice below how it says “with yield 0.92 percentage points above treasuries”.

We price bonds in this manner so we can understand and track the underlying investor feeling towards risk in any given market.

So in the example above, we said Apple priced their 2031 bonds at 1.70% and their 2061 bonds at 2.80%.

If we know they priced the “risk” of Apple bonds 92 basis points above Treasuries, we know the 10-year treasury then was 0.78% (1.70% - 0.92%) and the 40-year treasury was priced at 1.88% (2.80% - 0.92%).

The 0.92% is the price of the risk above treasuries. We can now easily track this pricing of risk over time, no matter what the yield on the US treasuries would be at that time.

And this risk can be tracked over time.

We use the option-adjusted spread (think the spread of the average bond is issued above treasuries) as a gauge of the health of the credit market and as a leading indicator of how equity markets may perform in the future.

If credit investors are looking to get paid more for risk, this means they see a higher probability of “bankruptcy” risk in the future.

In past business cycles, credit markets have led the equity markets in major downturns and upturns.

Once the bond is priced and the yield determined, it moves from being a new issue to trading on the secondary market.

The majority of you reading this will never see or go through the process I outlined above. This happens with large investors who can buy blocks of $1, $5, $10, $25, or $100 million dollar bond tranches.

If you invest in a bond mutual fund or ETF, this process is happening behind the scenes to participate in new bond offerings. Most of this happens without you ever knowing.

The only part of bond investing you probably know about is that of investing or selling bonds after they have been issued.

This involves what we call the secondary markets.

The Secondary Market:

Once bonds are priced the initial investor in those bonds may not want to hold their new bond for the full length of its maturity.

Because of this, there is an active market to buy and sell existing bonds. This market is called the secondary market.

Of the four inputs to a bond we outlined above, this is where the price of the bond fluctuates and is determined.

The price of the bond can vary depending on a number of inputs we will discuss next week.

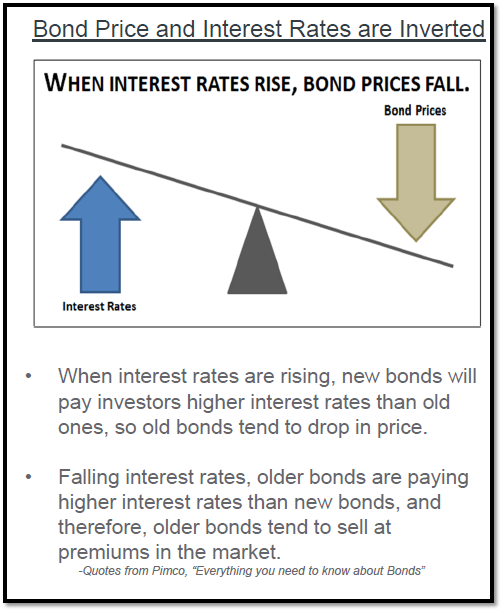

But no matter what type of bond we are talking about, when interest rates rise, the price of the bond falls.

Why do bond prices fall when rates increase?

Let’s go back to the Apple example we used above.

Let’s say Apple wanted to issue bonds today and the market wanted to price these bonds with the same exact risk as before at 0.92% over treasuries.

Today the US 10-year yield closed at 2.897%. We would add the 0.92% risk on top of this treasury yield and get a bond coupon of 3.82%.

In a matter of 6-months holding everything else constant except for the current US bond market rate, Apple would have to issue bonds today at 3.82% instead of the 1.70% it issued them 6-months ago.

Because of this move, how would an owner of the 1.70% Apple bonds sell those bonds in the market today?

We know the bond’s face value, coupon, and length are fixed. They cannot change. So the only way to adjust is the price of the bond.

Using a basic computer model below, we can quickly determine that this bond would have to sell at $83.98 per bond ($839.82) for a buyer to be interested in buying this bond in the market.

So in the middle of 2021, owners of the Apple bond purchased these bonds for $1,000 to receive a 1.70% of interest each year for the next 10 years.

IF that owner wanted to sell that bond today, they would have to sell it for $839.82, or a $160 loss, or a percentage loss of 16% !!!!

That is right….Owners of Apple Bonds are seeing a paper loss of 16% today on that bond!!!

This is just a paper loss. If that owner held their Apple bond till maturity, they would receive their initial $1,000 back. It is priced today lower to make up the difference between today’s yield and the yield we saw in the market 6 months ago.

Bond prices can also change because of the perceived risk of those bonds.

Using the Tesla example, if Tesla issued bonds in 2014 with risk over treasuries of say 600 basis points (6%), today this would be much low. As Tesla is in a much better financial position than it was in 2014, that risk is probably down to 200 basis points. So to adjust for the lowering of risk, the price of these bonds would move higher.

So all day everyday bond investors are monitoring two things:

The credit risk of their holdings and if it has changed and

the duration risk of their holds if they can get paid better at current rates for the same risk.

This is why Investment Grade Bonds have performed so poorly. There is no change in the companies or the risk but the big change we have seen in treasuries has created big decreases in the price of these bonds in the market just like we highlighted above with the Apple bonds.

Let’s take a quick look at returns over the past 18 months.

The Investment Grade Bond market is measured by the Barclays US Aggregate Bond index.

In 2021 it returns -1.54% !!!

Another measure of longer-term Investment Grade Bonds is The Barclays US Aggregate Government Long-Treasury Index.

In 2021 it returned -4.65%!!!

But look at how these returns broke down in the first quarter of 2022.

In the first quarter of 2022, the Barclays Us Aggregate Bond index returned -5.93%!!!

The Barclays US Aggregate Government Long-Treasury bond Index returned -10.58%!!!

Yes, you read that right.

What is used as the long-term risk-free asset class around the world has been down over 15% in the last 18 months!!!

This has nothing to do with credit risk but everything to do with duration risk (which we will discuss next week).

In 2021 the JP Morgan US High Yield Index returned +6.00% on the year.

In the first quarter of 2022, the JP Morgan US High Yield index was down -4.20%.

Clearly, it has paid to take credit risk versus duration risk over the past 18 months. (and if you continue to see me use duration and you have no idea what this means, do not worry…by end of next week you will be an expert).

This is because we have seen a fantastic economy, great growth, and the best employment market in two generations.

In that type of market, even the worst companies in the world do well.

Next week we will discuss duration risk which is the main driver of these returns over the last 18 months, what you should know about different vehicles in basic fixed income to invest in, and how to think about investing in fixed income moving forward to not get smoked on your returns.

Have a wonderful weekend.